How to Apply for a Home Loan as a Self-Employed Borrower

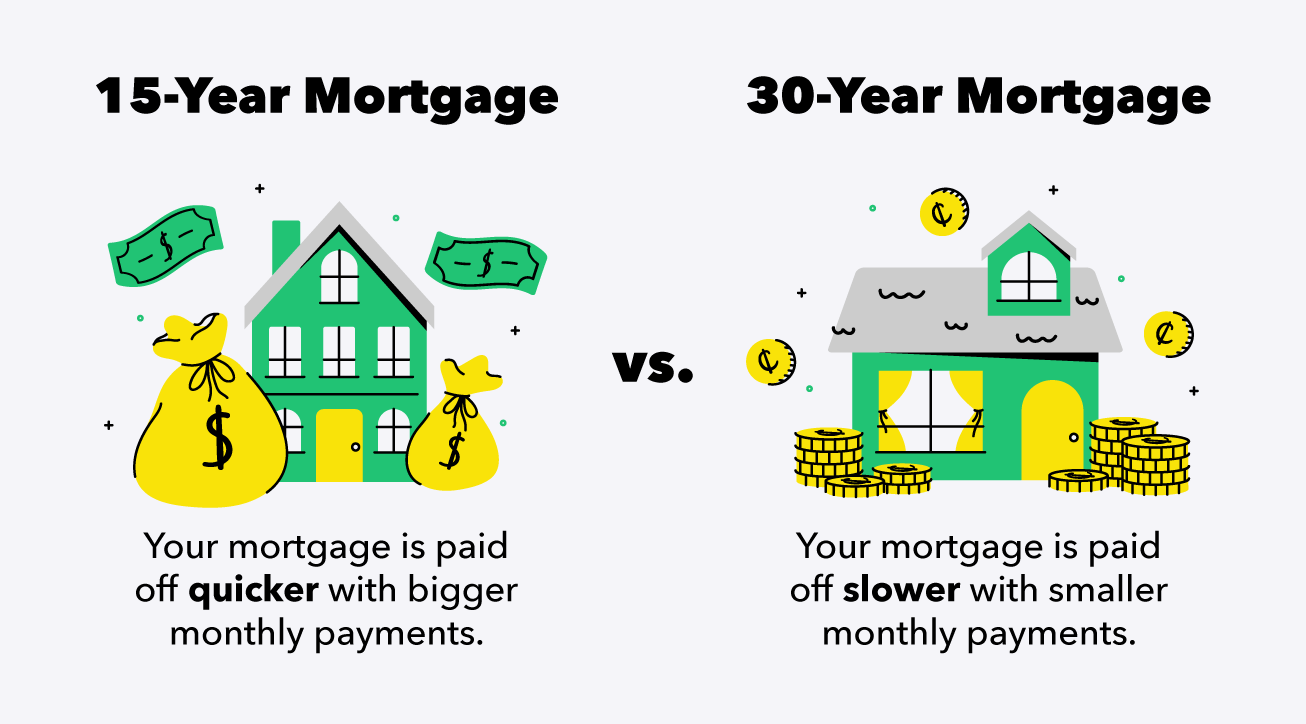

Should You Consider a 15-Year vs. 30-Year Home Loan?

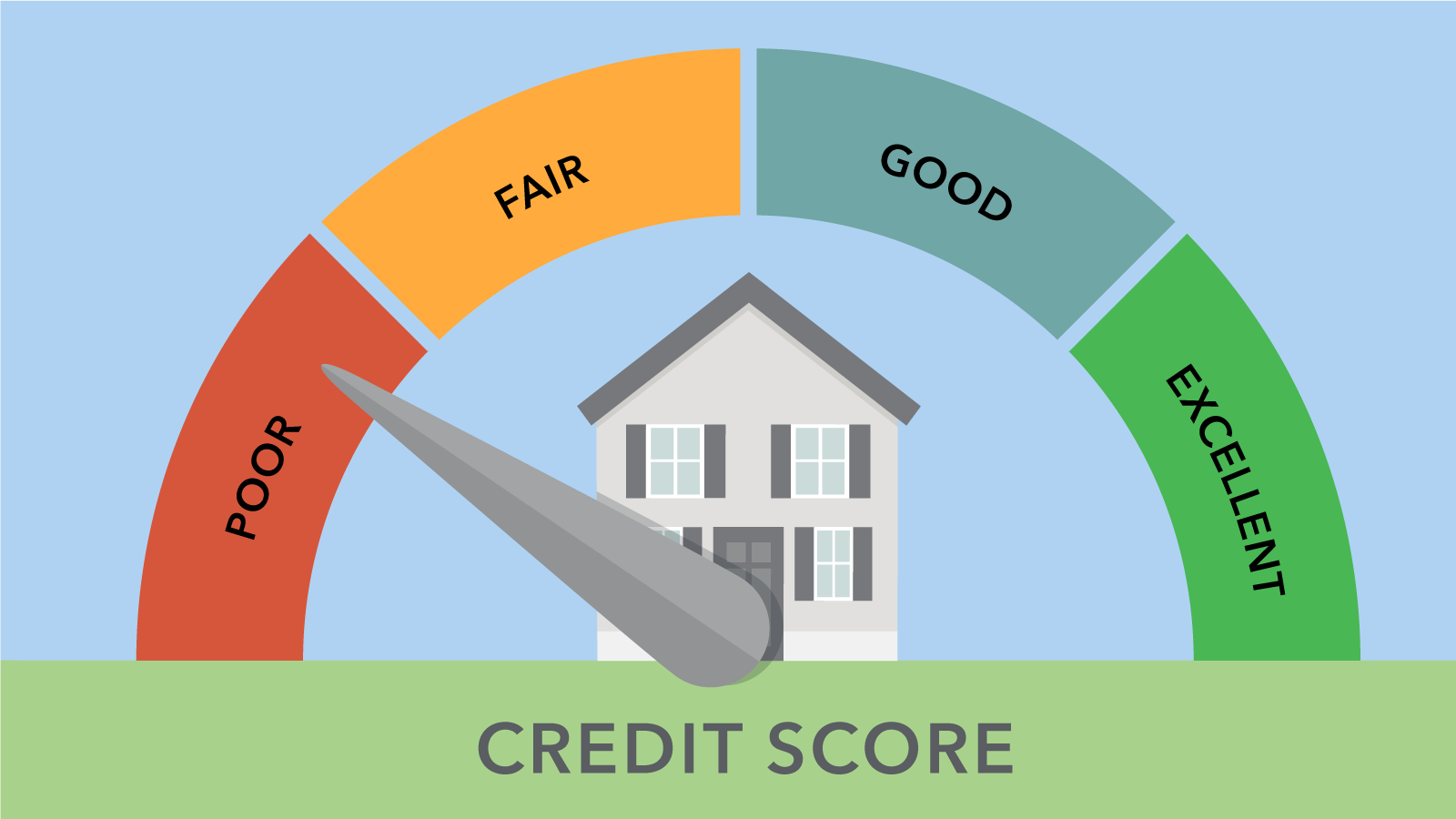

How to Secure a Home Loan With a Low Credit Score

How to Secure a Home Loan With a Low Credit Score – Buying a home is a big milestone, but if your credit score is less than ideal, the process can feel overwhelming. Many people assume that a low credit score automatically disqualifies them from getting a mortgage. The truth is, that’s not always the case. There are still ways to secure a home loan with a low credit score, as long as you understand your options and prepare strategically.

Lenders look at more than just your credit score. While your score plays an important role in determining your eligibility and interest rate, it is only one part of the overall picture. Income stability, debt-to-income ratio, employment history, and the size of your down payment also matter. If you approach the process wisely, you can increase your chances of approval even with less-than-perfect credit.

Understanding How Credit Score Affects Your Mortgage

Your credit score is a numerical representation of your creditworthiness. It tells lenders how reliable you have been in repaying debts. Most conventional lenders prefer borrowers with scores above 620, but this does not mean lower scores are automatically rejected.

For example, loans backed by the Federal Housing Administration are designed to help borrowers with lower credit scores. FHA loans often allow credit scores as low as 580, and sometimes even lower with a larger down payment. This makes them a popular option for first-time homebuyers who may not have strong credit histories.

On the other hand, conventional loans typically follow guidelines set by Fannie Mae and Freddie Mac. These institutions usually require higher credit scores and stricter financial qualifications. However, each lender has its own criteria, so shopping around is essential.

A lower credit score generally means higher interest rates. This is because lenders see you as a higher risk. Over the life of a mortgage, even a small difference in interest rate can significantly affect how much you pay. That’s why it’s important to explore strategies that can improve your application strength before applying.

Practical Steps to Secure a Home Loan With a Low Credit Score

Getting approved for a mortgage with a low credit score is possible if you take the right steps. Preparation and planning can make a huge difference in how lenders view your application.

Review and Improve Your Credit Before Applying

Before you start applying for a home loan, check your credit report carefully. Look for errors such as incorrect late payments, duplicate accounts, or debts that have already been paid. Disputing inaccuracies can sometimes boost your score faster than you expect.

If possible, spend a few months improving your credit. Pay all bills on time, reduce credit card balances, and avoid opening new lines of credit. Even a small increase in your score can qualify you for better mortgage terms.

Consistency matters more than quick fixes. Lenders want to see stable financial behavior. Showing several months of on-time payments can strengthen your case, even if your score is still below average.

Save for a Larger Down Payment

One of the most effective ways to secure a home loan with a low credit score is by offering a larger down payment. A higher down payment reduces the lender’s risk because you are borrowing less money. It also demonstrates financial responsibility.

If you can put down 10% to 20% instead of the minimum requirement, lenders may be more willing to work with you. In some cases, a larger down payment can even offset the impact of a lower credit score when determining your interest rate.

Saving more upfront also reduces your monthly mortgage payments and may help you avoid private mortgage insurance, depending on the loan type.

Lower Your Debt-to-Income Ratio

Your debt-to-income ratio, often called DTI, measures how much of your monthly income goes toward paying debts. Lenders use this ratio to evaluate whether you can afford a mortgage payment.

If you have a low credit score, lowering your DTI can strengthen your application. Focus on paying off smaller debts such as credit cards or personal loans. Avoid taking on new debt before applying for a home loan.

A lower DTI shows lenders that you are not financially overextended. This can increase your chances of getting approved even if your credit score is less than ideal.

Exploring Loan Options for Low Credit Borrowers

Not all mortgage products are created equal. Some are specifically designed to help borrowers with lower credit scores achieve homeownership.

FHA loans, backed by the Federal Housing Administration, are among the most popular options. They offer more flexible credit requirements and lower down payment options compared to conventional loans. However, they do require mortgage insurance premiums, which add to the overall cost.

Another potential option is a VA loan, guaranteed by the U.S. Department of Veterans Affairs. These loans are available to eligible veterans, active-duty service members, and certain military spouses. VA loans often have no minimum credit score requirement set by the agency, though individual lenders may impose their own standards.

USDA loans, supported by the U.S. Department of Agriculture, are designed for rural and suburban homebuyers who meet income requirements. These loans can offer low interest rates and zero down payment options, making them attractive to borrowers with moderate or lower credit scores.

Each program has specific eligibility requirements, so it’s important to research which one fits your financial situation and long-term goals.

Work With the Right Lender

When trying to secure a home loan with a low credit score, choosing the right lender can make a significant difference. Some lenders specialize in working with borrowers who have less-than-perfect credit. They may offer more flexible underwriting standards or provide guidance on improving your application before submission.

It’s wise to compare multiple lenders and request pre-approval quotes. This allows you to see potential interest rates and loan terms without committing immediately. Make sure to ask about all associated costs, including closing fees and mortgage insurance.

Building a relationship with a knowledgeable loan officer can also help. An experienced professional can suggest specific actions to improve your approval chances and recommend loan programs suited to your profile.

Consider a Co-Signer or Alternative Strategies

If your credit score is too low to qualify on your own, adding a co-signer with stronger credit may help. A co-signer agrees to share responsibility for the loan, which reduces the lender’s risk.

However, this is a serious commitment. If you fail to make payments, your co-signer’s credit will also be affected. Make sure both parties fully understand the responsibilities involved before moving forward.

Another strategy is to delay your home purchase and focus on rebuilding your credit. While this requires patience, it can save you thousands of dollars in interest over the life of the loan.

Final Thoughts on Securing a Home Loan With a Low Credit Score

Securing a home loan with a low credit score is not impossible. It requires preparation, realistic expectations, and a willingness to explore alternative mortgage options. By improving your credit habits, saving for a larger down payment, lowering your debt-to-income ratio, and choosing the right loan program, you can significantly increase your chances of approval.

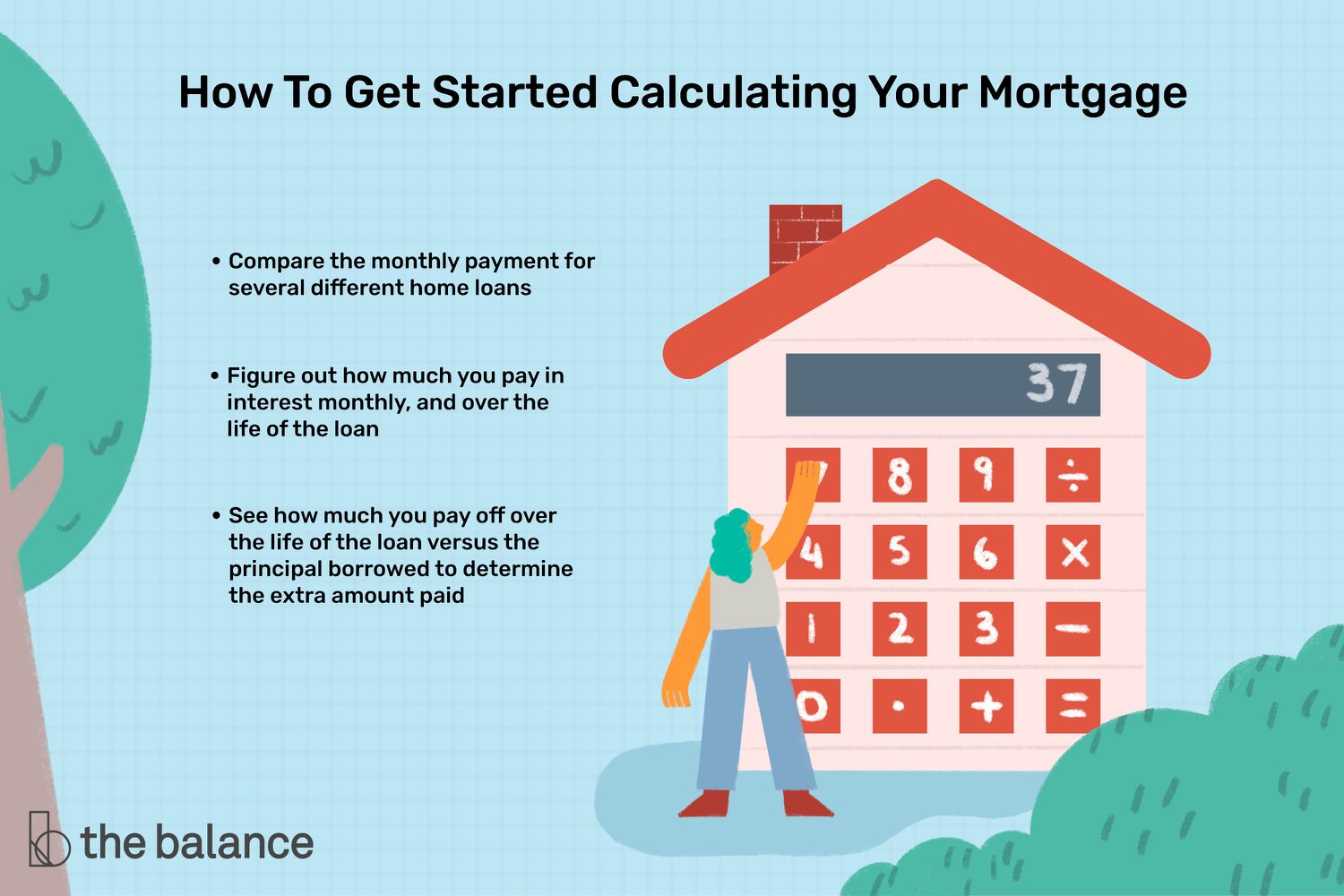

How to Use a Home Loan Calculator to Estimate Your Payments

How to Use a Home Loan Calculator to Estimate Your Payments – Buying a home is an exciting milestone, but understanding the financial commitment can sometimes feel overwhelming. One of the easiest ways to get a clearer picture of your potential mortgage is by using a home loan calculator. These tools provide an estimate of your monthly payments, helping you plan your budget and make informed decisions. By knowing what to expect, you can approach the home-buying process with confidence and clarity.

What is a Home Loan Calculator?

A home loan calculator is an online tool that estimates your monthly mortgage payments based on factors such as loan amount, interest rate, loan term, and down payment. It can also factor in additional costs like property taxes and homeowners insurance, giving you a comprehensive view of what your monthly obligations might look like. While it doesn’t replace professional financial advice, a calculator provides a helpful starting point for planning and budgeting.

Using a calculator allows you to test different scenarios. For example, you can see how increasing your down payment, reducing your loan term, or adjusting the interest rate affects your monthly payments. This flexibility is invaluable when comparing loan options and understanding how small changes can make a big difference over time.

Why Using a Home Loan Calculator Matters

Understanding your potential mortgage payments is essential for making informed financial decisions. A calculator helps you avoid overextending yourself and ensures you choose a loan that fits your budget. It also allows you to plan for related expenses, such as property taxes, insurance, and maintenance, so there are no surprises once you move in.

Additionally, using a calculator can strengthen your position when negotiating with lenders. By knowing how different terms affect your monthly payments, you can confidently discuss rates, repayment options, and loan terms. It helps you approach the process strategically rather than relying solely on the lender’s guidance.

How to Use a Home Loan Calculator

Using a home loan calculator is straightforward, but it’s important to input accurate information to get reliable estimates. Here’s a step-by-step guide to using one effectively.

Step 1: Enter the Loan Amount

The loan amount is the total money you plan to borrow from the lender. It is usually the price of the property minus your down payment. For example, if the home costs $300,000 and you are putting down $60,000, your loan amount would be $240,000. Accurately entering this figure ensures the calculator provides a realistic estimate of your monthly payments.

Step 2: Input the Interest Rate

The interest rate is a key factor in determining your monthly payments. Even a small difference in rates can have a significant impact over the life of the loan. Be sure to use the current rate offered by your lender or a rate you are likely to qualify for based on your credit profile. Many calculators allow you to test different interest rates to see how they affect your payments.

Step 3: Choose the Loan Term

The loan term is the length of time you have to repay the mortgage, typically 15, 20, or 30 years. Shorter terms usually mean higher monthly payments but less interest paid over time, while longer terms reduce monthly payments but increase total interest. By adjusting the loan term in the calculator, you can find a balance between affordable monthly payments and minimizing total interest.

Step 4: Include Additional Costs

Some home loan calculators allow you to include property taxes, homeowners insurance, and mortgage insurance. These costs can significantly impact your monthly payments, so including them provides a more realistic estimate. Even if your calculator does not have this option, be sure to account for these expenses separately when planning your budget.

Step 5: Review and Adjust

Once you enter all the details, the calculator will provide an estimate of your monthly payment. Take time to review the result and experiment with different scenarios. For instance, increasing your down payment or slightly adjusting the interest rate can lower your payments. Testing different options helps you understand the flexibility you have and identify the most manageable mortgage for your situation.

Benefits of Using a Home Loan Calculator

Home loan calculators offer several advantages for prospective borrowers. They simplify complex calculations, allowing you to focus on other aspects of the home-buying process. They also help you:

-

Plan your budget accurately. Knowing your estimated monthly payments prevents overspending.

-

Compare loan options. Calculators allow you to see how different rates, terms, and down payments affect payments.

-

Negotiate with lenders. Being informed gives you leverage when discussing loan terms.

-

Reduce stress. Understanding your potential financial commitment makes the home-buying process less overwhelming.

By providing clarity and insight, calculators empower you to make decisions with confidence rather than relying on guesswork.

Tips for Maximizing Accuracy

While home loan calculators are useful, accuracy depends on the information you provide. Here are a few tips to get the most out of these tools:

-

Use realistic numbers. Base your inputs on actual quotes from lenders rather than estimates.

-

Factor in all costs. Don’t forget taxes, insurance, and potential maintenance expenses.

-

Check multiple calculators. Different calculators may use slightly different formulas, so comparing results can give you a more accurate range.

-

Update numbers regularly. Interest rates, property prices, and personal finances change over time, so recalculate if any key variables change.

When to Use a Home Loan Calculator

A home loan calculator is helpful at multiple stages of the home-buying process. Initially, it helps you set a budget and determine what price range you can afford. Later, it allows you to compare different loan offers and see how varying interest rates or terms affect your payments. Even after securing a mortgage, it can help you plan for refinancing options or paying off your loan faster.

Using a calculator early and often ensures you make informed decisions every step of the way. It’s a simple tool that can prevent costly mistakes and make your financial planning more precise.

Final Thoughts: Empower Your Home-Buying Decisions

Estimating your home loan payments is a crucial step in achieving a successful and stress-free home purchase. A home loan calculator provides a clear view of your potential monthly payments, helping you budget, compare loan options, and negotiate effectively with lenders. By entering accurate information and testing different scenarios, you can gain confidence in your decisions and choose a mortgage that aligns with your financial goals.

Whether you are a first-time homebuyer or an experienced investor, taking the time to use a home loan calculator ensures that you understand the full scope of your financial commitment. It’s a small step that can have a big impact on your long-term financial well-being, turning what might feel like a complicated process into an empowering and manageable experience.

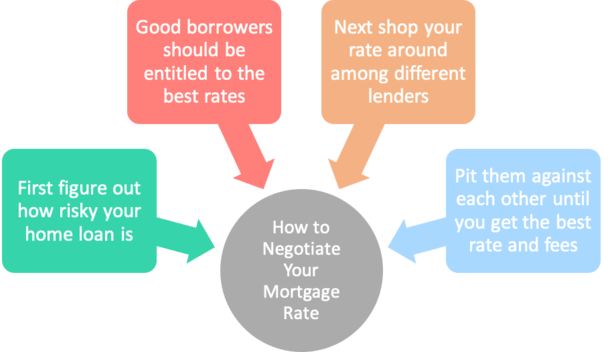

How to Negotiate Your Home Loan Terms With Lenders

How to Negotiate Your Home Loan Terms With Lenders – Buying a home is one of the biggest financial decisions most people will make in their lifetime. While finding the perfect property is exciting, negotiating the terms of your home loan is equally important. Many borrowers accept the first loan offer they receive, but understanding how to negotiate with lenders can save you thousands of dollars over the life of the mortgage. With the right approach, preparation, and knowledge, you can secure favorable interest rates, lower fees, and flexible repayment options that suit your financial goals.

Why Negotiating Your Home Loan Matters

A home loan is a long-term commitment, often lasting 15 to 30 years. Even a small reduction in interest rates or fees can make a significant difference in your monthly payments and total interest paid. Negotiating your loan terms allows you to gain control over costs, reduce financial stress, and customize your mortgage to fit your needs. Lenders often have some flexibility, especially for borrowers with strong credit scores, stable income, and a clear understanding of the market. Knowing your leverage and approaching the conversation strategically can put you in a strong position.

Understand Your Financial Position

Before entering negotiations, it’s essential to have a clear picture of your financial situation. Lenders will consider your credit score, income, debt-to-income ratio, and employment stability when determining the terms of your loan. By reviewing your finances in advance, you can identify areas that may improve your negotiation power. For instance, paying down high-interest debts or correcting errors on your credit report can boost your creditworthiness. Understanding your finances also helps you determine the type of mortgage you can realistically afford and the monthly payments that fit your budget.

Check Your Credit Score

Your credit score is one of the most critical factors in home loan negotiations. Lenders use it to assess risk and decide on interest rates. A higher credit score often translates into lower rates and more favorable terms. Before negotiating, check your credit report for inaccuracies, pay down outstanding balances, and avoid taking on new loans. Demonstrating financial responsibility can increase a lender’s willingness to offer better terms.

Compare Loan Offers

Not all lenders offer the same rates or conditions, so shopping around is a key step in negotiation. Comparing multiple loan offers gives you leverage when discussing terms with your preferred lender. By showing that you have options, you signal that you are an informed borrower and can walk away if terms are not favorable. Pay attention to interest rates, origination fees, closing costs, and repayment flexibility when evaluating offers. Even small differences in rates can save you significant amounts over the life of your mortgage.

Consider Different Loan Types

Lenders provide a variety of loan options, including fixed-rate, adjustable-rate, and interest-only mortgages. Each type comes with different benefits and risks. Understanding the options allows you to negotiate terms that align with your long-term financial goals. For example, a fixed-rate mortgage offers predictable monthly payments, while an adjustable-rate mortgage may provide lower initial rates but can fluctuate over time. Being informed about these differences strengthens your position in discussions with lenders.

Be Prepared to Ask

Negotiation is not just about waiting for the lender to offer better terms—it involves proactive questions. Ask about interest rate reductions, lower origination fees, or the possibility of waiving certain closing costs. Some lenders may also offer flexible repayment schedules or discounts for automatic payments. By initiating the conversation, you demonstrate that you are an engaged borrower who understands the value of the loan. Lenders may be more willing to accommodate requests when they see that you are serious, organized, and financially responsible.

Leverage Your Strengths

Your financial profile can serve as a powerful tool in negotiation. Stable income, a high credit score, a sizable down payment, or a long-standing relationship with a bank can all be used to your advantage. Highlight these strengths during discussions with your lender. For example, offering a larger down payment might encourage the lender to lower your interest rate, as it reduces their risk. Demonstrating reliability and preparedness can make lenders more flexible in offering favorable terms.

Understand Lender Incentives

Lenders often have incentives to attract borrowers, such as reduced fees for refinancing, special rates for certain customer groups, or promotions for first-time homebuyers. By researching these incentives, you can identify opportunities to negotiate. Understanding what motivates a lender helps you frame your requests in a way that aligns with their goals. This approach can increase the likelihood of achieving better terms without pushing too hard or risking the relationship.

Don’t Rush the Process

Negotiating a home loan is not something to be rushed. Take the time to review offers, ask questions, and understand the implications of different terms. Rushing may lead to missing hidden fees, unfavorable conditions, or long-term costs. Patience allows you to weigh your options carefully and enter discussions with confidence. A well-considered approach shows lenders that you are informed and serious, which can make them more willing to negotiate.

Seek Professional Advice

If you’re unsure about the negotiation process, consider consulting a mortgage broker or financial advisor. Professionals can provide insights into market trends, lender practices, and optimal strategies for negotiation. Their expertise can help you navigate complex loan documents and identify opportunities that might not be immediately apparent. While professional advice may come at a cost, the potential savings from securing better loan terms often outweigh the expense.

Final Thoughts: Negotiation is Key to Savings

Negotiating your home loan terms is an essential step in responsible homeownership. By understanding your financial position, comparing offers, asking informed questions, and leveraging your strengths, you can secure a mortgage that works for you. Lenders have flexibility, and informed borrowers who take the time to negotiate often enjoy lower rates, reduced fees, and more favorable conditions.

Remember, a home loan is a long-term commitment, and every dollar saved in interest or fees matters. Approaching negotiations strategically not only reduces financial strain but also empowers you to make decisions that align with your long-term goals. With preparation, knowledge, and confidence, you can turn the home loan process into an opportunity to gain financial advantage rather than simply a necessary step in buying a property.

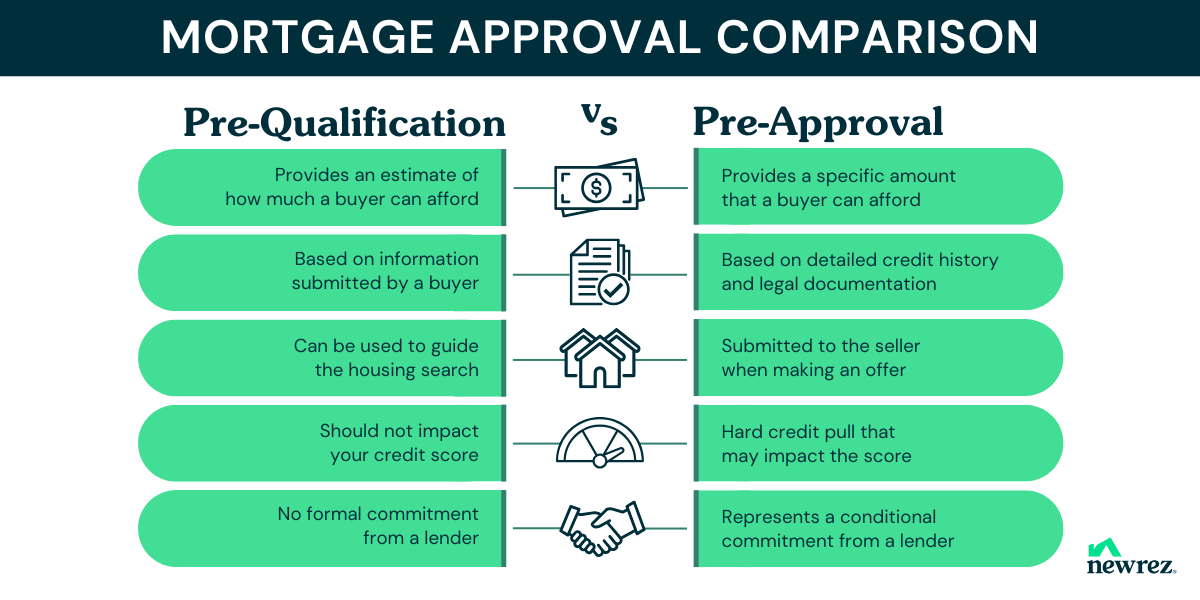

Understanding Loan Pre-Approval vs. Pre-Qualification

Understanding Loan Pre-Approval vs. Pre-Qualification – Buying a home, purchasing a car, or securing a personal loan can be a complex journey. One of the first steps that often confuses people is understanding the difference between loan pre-approval and pre-qualification. While both processes help borrowers gauge how much they might be able to borrow, they serve different purposes and carry different weight with lenders. Knowing the difference can make your borrowing experience smoother and increase your chances of getting the loan you need.

What is Loan Pre-Qualification?

Loan pre-qualification is typically the first step in the borrowing process. It is an informal assessment where a lender reviews basic financial information to estimate how much you might be eligible to borrow. During pre-qualification, you may provide details about your income, debts, assets, and credit history, but this process often does not involve a hard credit check.

Pre-qualification gives borrowers a rough idea of the loan amount they could qualify for. It’s useful for budgeting and planning, especially when shopping for a home or comparing lenders. However, it’s important to understand that pre-qualification does not guarantee loan approval. Lenders can provide an estimate, but until you go through more detailed checks, nothing is final.

Benefits of Pre-Qualification

Pre-qualification is convenient and quick. It helps borrowers understand what loan products may suit their financial situation without committing to a formal application. For first-time homebuyers or anyone exploring financing options, it offers a clear starting point. Since the process is informal, it usually doesn’t affect your credit score, making it a low-risk way to explore your borrowing potential.

What is Loan Pre-Approval?

Loan pre-approval is a more formal and in-depth process. Unlike pre-qualification, pre-approval requires a detailed review of your financial history and often includes a hard credit check. Lenders will verify your income, employment status, debts, and assets, and may request supporting documentation such as tax returns, pay stubs, and bank statements.

Once pre-approved, you receive a conditional commitment from the lender stating the maximum loan amount they are willing to offer. This conditional approval is usually valid for a limited time, giving you a clear understanding of your budget when making major purchases like buying a house. Pre-approval shows sellers and lenders that you are a serious borrower, which can be an advantage in competitive markets.

Advantages of Pre-Approval

Pre-approval provides certainty and confidence. Knowing exactly how much you can borrow allows you to focus your search on options within your budget. It also gives you negotiating power with sellers, as they can see that you have secured financing. For buyers in fast-moving markets, pre-approval can be the difference between winning a bid and missing out on a property.

When to Consider Pre-Qualification

Pre-qualification is ideal for those just beginning their borrowing journey or exploring their options. If you are unsure about your financial readiness or want to compare different lenders, pre-qualification can give you a clear starting point. It’s also helpful for understanding what loan products you might qualify for, which can guide your financial planning.

For example, a first-time homebuyer might seek pre-qualification to determine how much house they can afford. This step allows them to refine their budget and focus on properties within their financial reach without the pressure of a formal application.

When to Consider Pre-Approval

Pre-approval is the logical next step when you are serious about making a purchase. If you are ready to start house hunting, buy a car, or make any significant financial commitment, pre-approval provides a stronger position. Sellers and lenders take pre-approved buyers more seriously, and you gain clarity on your budget and loan terms.

In competitive markets, pre-approval can speed up the purchasing process and prevent delays. Since the lender has already verified your financial situation, closing a deal can be faster once you make an offer. This makes pre-approval especially valuable in real estate or high-demand vehicle purchases.

Tips for a Smooth Pre-Approval Process

-

Check Your Credit Score: Before applying, ensure your credit report is accurate. Correcting errors can improve your chances of approval.

-

Gather Documentation: Prepare pay stubs, tax returns, bank statements, and other financial records in advance.

-

Reduce Debt: Lowering your debt-to-income ratio can increase the loan amount you are eligible for.

-

Avoid New Credit Applications: Taking on new loans or credit cards can affect your pre-approval outcome.

Following these steps can make the pre-approval process faster, smoother, and more likely to result in favorable loan terms.

Conclusion: Choosing the Right Step for Your Situation

Understanding the difference between pre-qualification and pre-approval is crucial for any borrower. Pre-qualification provides a helpful overview of your borrowing potential without commitments, while pre-approval offers a verified and conditional loan amount that strengthens your position in financial negotiations. By knowing when and how to use each option, you can plan your purchases more effectively, make informed financial decisions, and increase your chances of securing the loan you need.

Whether you are entering the housing market for the first time or planning a major purchase, starting with pre-qualification and moving to pre-approval ensures that you approach the process with confidence and clarity. Taking these steps strategically can save time, reduce stress, and ultimately help you achieve your financial goals.

Home Loan Trends from the Past Property Era

2026 Home Loan Tips: Trends, Rates & Application Hacks

2026 Home Loan Tips: Trends, Rates & Application Hacks – The home loan landscape in 2026 looks very different compared to just a few years ago. Buyers are more informed, lenders are more selective, and technology is deeply embedded in almost every step of the mortgage process. Whether you’re a first-time buyer or someone looking to refinance, understanding how home loans work in 2026 can save you thousands of dollars and months of frustration.

This guide breaks down the latest home loan trends, what to expect from interest rates, and practical application hacks that can improve your approval chances.

The Home Loan Market in 2026

The housing market has matured after years of volatility. In 2026, stability is the keyword most lenders and borrowers are using. While prices are no longer skyrocketing overnight, demand for housing remains strong in most regions.

Banks and non-bank lenders have adjusted their strategies. Risk assessments are tighter, but competition between lenders is still alive. This balance creates opportunities for borrowers who come prepared.

Digital-First Mortgage Processes

One of the biggest shifts in 2026 is how digital the home loan journey has become. Paper-based applications are nearly gone. Most lenders now use automated income verification, open banking data, and AI-powered credit assessments.

For borrowers, this means faster approvals, but also less room for inconsistencies. Any mismatch in your financial data can raise red flags instantly. Accuracy matters more than ever.

Home Loan Interest Rates: What to Expect in 2026

Interest rates in 2026 are relatively stable compared to the aggressive hikes seen in earlier years. Central banks have shifted focus from inflation control to economic balance, which has helped calm rate fluctuations.

That said, rates are not identical across lenders, and the gap between advertised rates and approved rates can be significant.

Fixed vs Variable Loans in 2026

Fixed-rate home loans are popular among borrowers who value predictability. In 2026, fixed terms are often shorter, commonly two to three years, giving borrowers flexibility to refinance if market conditions improve.

Variable-rate loans remain attractive for those comfortable with moderate risk. Many lenders now offer hybrid products that allow partial fixing while keeping the rest variable, giving borrowers more control over their repayments.

Credit Score Impact on Your Rate

Your credit score still plays a massive role in determining your interest rate. In 2026, lenders rely heavily on behavioral data, not just traditional credit reports. Payment consistency, account balances, and spending patterns can all influence your final rate.

Improving your credit profile even six months before applying can make a noticeable difference in loan pricing.

Home Loan Application Hacks That Actually Work

Applying for a home loan in 2026 is less about luck and more about preparation. Small adjustments before submitting your application can dramatically improve your approval odds.

Clean Up Your Financial Profile Early

Lenders typically analyze at least six to twelve months of financial history. Reducing unnecessary subscriptions, avoiding impulsive purchases, and keeping stable balances sends a strong signal of reliability.

Job stability also matters. Frequent job changes may not disqualify you, but lenders prefer consistent income streams, especially for higher loan amounts.

Lower Your Debt-to-Income Ratio

One of the most overlooked factors in home loan approval is the debt-to-income ratio. Even if your income is high, excessive existing debt can limit how much you can borrow.

Paying down credit cards, personal loans, or buy-now-pay-later balances before applying can unlock better loan terms and higher borrowing capacity.

Get Pre-Approval the Smart Way

Pre-approval is still a powerful tool in 2026, but it needs to be done carefully. Multiple pre-approval checks across different lenders can hurt your credit score.

Working with a mortgage broker or shortlisting two or three lenders before applying helps reduce unnecessary credit inquiries while still giving you options.

Refinancing Trends in 2026

Refinancing is no longer just about chasing lower rates. In 2026, homeowners refinance to restructure debt, access equity, or switch to more flexible loan products.

Many lenders offer streamlined refinancing processes with minimal documentation for borrowers with strong repayment histories. This makes refinancing faster and cheaper than ever before.

When Refinancing Makes Sense

Refinancing can be a smart move if your financial situation has improved, property value has increased, or your current loan features no longer fit your needs.

However, refinancing solely for a small rate reduction may not always be worth it once fees and reset terms are considered. Running the numbers carefully is essential.

Common Home Loan Mistakes to Avoid

Despite easier access to information, many borrowers still make avoidable mistakes during the home loan process.

Overestimating borrowing capacity is a common issue. Just because a lender approves a certain amount does not mean it fits your lifestyle or long-term goals.

Another frequent mistake is ignoring loan features. Offset accounts, redraw facilities, and repayment flexibility can have a bigger impact over time than a slightly lower interest rate.

How to Position Yourself for Success in 2026

The most successful borrowers in 2026 treat home loans as a long-term financial strategy, not just a transaction. They plan ahead, understand lender expectations, and remain flexible.

Staying informed about market trends, reviewing your loan regularly, and maintaining a healthy financial profile will keep you in a strong position whether you’re buying, refinancing, or investing.

Final Thoughts on Home Loans in 2026

Home loans in 2026 are faster, smarter, and more data-driven than ever before. While the process may seem strict, borrowers who prepare properly can access competitive rates and flexible loan structures.

Understanding current trends, keeping an eye on interest rate movements, and applying smart financial habits will give you a clear advantage. In a market where lenders value transparency and consistency, being prepared is the ultimate application hack.

Home Loans That Haunt: Debt Traps and Long-Term Burdens

Home Loans That Haunt: Debt Traps and Long-Term Burdens – Buying a home is often seen as a milestone of financial success and stability. For many, taking out a home loan is the only way to make this dream a reality. However, not all home loans are created equal. Some loans, despite appearing manageable at first, can quickly turn into debt traps, leaving homeowners with long-term financial burdens that are difficult to escape.

Understanding how these loans work, why they become problematic, and how to avoid them is essential for anyone considering borrowing to buy a home. This guide explores the risks of debt-heavy home loans and offers practical advice for making safer, smarter choices.

How Home Loans Can Become Debt Traps

At first glance, a home loan may seem like a straightforward way to buy property. The monthly payments appear manageable, and lenders often highlight attractive features like low initial interest rates. But hidden costs, complex terms, and poor financial planning can turn a seemingly good deal into a long-term nightmare.

Debt traps often start with loans that offer minimal payments at the beginning but balloon over time. Adjustable rates, deferred interest, or interest-only periods can leave borrowers facing unexpectedly high repayments in the future. Without careful planning, these loans become burdens that stretch over decades, affecting personal finances, savings, and lifestyle.

The Role of High-Interest and Hidden Fees

Many homeowners underestimate how interest and fees accumulate over time. Even a small difference in interest rates can result in thousands of dollars paid over the life of the loan. Some lenders also include hidden charges for administrative costs, early repayments, or late fees, which compound financial stress.

Loans with variable or adjustable rates carry the additional risk of increasing payments. A sudden rise in interest can push monthly installments beyond what the borrower can comfortably manage, leading to late payments, penalties, and long-term debt accumulation.

Common Characteristics of Risky Home Loans

Not every home loan carries the same risk. Certain types of loans are more likely to create financial burdens that last for decades. Recognizing these characteristics can help buyers avoid falling into a debt trap.

Interest-Only and Low-Initial Payment Loans

Interest-only loans allow borrowers to pay just the interest for a set period, usually a few years. While this reduces monthly payments initially, it does not reduce the principal amount borrowed. When the interest-only period ends, payments increase dramatically, catching many borrowers off guard.

Loans with low initial payments may also be marketed as “affordable” options. However, once promotional rates expire, monthly repayments rise significantly, creating financial strain.

Loans With Complex Terms and Fine Print

Some home loans come with clauses that are difficult to understand but have significant long-term consequences. Adjustable-rate loans, balloon payments, and variable fees are common examples. Borrowers who fail to fully grasp these terms may find themselves unprepared for sudden repayment hikes or additional charges.

Lenders often disclose these terms, but in fine print that many people overlook. Carefully reviewing loan agreements and asking questions before signing can prevent unexpected debt traps.

Planning Ahead to Avoid Long-Term Financial Burdens

Avoiding debt traps starts before signing any loan agreement. Planning, research, and realistic assessment of financial capacity are key. Understanding both the short-term and long-term implications of a loan ensures that homeownership remains a positive experience rather than a burden.

Budgeting for True Costs of Homeownership

Monthly repayments are only part of the financial picture. Taxes, insurance, maintenance, and unexpected repairs all add to the cost of owning a home. Borrowers who plan their budgets with these factors in mind are better equipped to manage repayments even if interest rates increase.

A detailed financial plan also helps determine what size of loan is realistically manageable. It may mean borrowing less than the maximum the bank offers, but it prevents financial strain over the long term.

Improving Credit and Financial Health

A strong credit profile not only increases approval chances but also helps secure lower interest rates. High debt-to-income ratios, poor credit history, or unstable income can push borrowers toward higher-risk loans with unfavorable terms.

Taking time to pay down existing debts, improving credit scores, and maintaining consistent income can make a significant difference in securing safer, more affordable home loans.

Red Flags to Watch Out For

Certain warning signs indicate that a home loan may become a long-term burden. Recognizing these early can save borrowers from years of financial stress.

High-interest rates that are significantly above market averages, loans requiring frequent adjustments, or offers with complex repayment schedules are common red flags. Additionally, loans that promise unusually low initial payments often come with hidden costs or future spikes in repayment.

Consulting with a financial advisor or mortgage expert can provide clarity. They can help evaluate whether a loan is sustainable or if it carries risks that outweigh short-term benefits.

Strategies to Escape or Avoid Debt Traps

For those already facing challenging home loan terms, there are strategies to mitigate long-term burdens. Refinancing, consolidating debts, or switching to fixed-rate loans can reduce monthly payments and provide stability. Early repayment of high-interest loans, if financially feasible, also lowers long-term costs.

Education and awareness are the best preventative strategies. Borrowers who take time to understand loan terms, anticipate future financial changes, and plan accordingly are far less likely to fall into debt traps.

Choosing Loans That Align With Long-Term Goals

A home loan should support long-term financial stability rather than create ongoing stress. Choosing loans with predictable payments, transparent fees, and terms that match income and lifestyle ensures a manageable repayment journey.

Flexible repayment options, the ability to make extra payments without penalties, and loans that avoid sudden spikes in costs help homeowners maintain financial control. Thinking beyond short-term affordability prevents the haunting burden of long-term debt.

Final Thoughts on Home Loans and Financial Responsibility

Homeownership should be a step toward financial growth and security, not a lifelong debt trap. Understanding the risks, planning carefully, and choosing loans wisely are essential to prevent long-term burdens.

Loans that appear affordable at first may hide future challenges. By budgeting realistically, improving financial health, and analyzing loan terms thoroughly, borrowers can make choices that protect their future and allow homeownership to remain a rewarding experience.

Being proactive and informed transforms borrowing from a potential liability into a strategic investment. Awareness, planning, and caution are the keys to escaping debt traps and building a home that is truly a place of comfort, not financial worry.

Property Financing Guide Mortgages Planning and Approval

Home Loan Guide for Real Estate Financing

Home Loan Guide for Real Estate Financing – Buying property is one of the biggest financial decisions most people will ever make. Whether you are purchasing your first home, upgrading to a larger space, or investing in real estate, understanding how home loans work is essential. This home loan guide for real estate financing is designed to help you navigate the basics in a clear and practical way, without overwhelming technical jargon.

A home loan is more than just borrowing money from a bank. It is a long-term financial commitment that affects your cash flow, lifestyle, and future plans. Knowing how the process works can save you money, reduce stress, and help you make smarter decisions in the property market.

Understanding Home Loans in Real Estate Financing

A home loan, also known as a mortgage, is a type of financing used to purchase or refinance real estate. The property itself usually acts as collateral, which allows lenders to offer lower interest rates compared to unsecured loans.

Most home loans are repaid over a long period, commonly ranging from 15 to 30 years. During this time, borrowers pay monthly installments that include both principal and interest. The exact structure depends on the loan type, interest rate, and lender policies.

How Home Loans Support Property Buyers

Real estate prices continue to rise in many markets, making it difficult for buyers to pay in cash. Home loans make property ownership possible by spreading the cost over time. This allows buyers to enter the market sooner while maintaining liquidity for other expenses or investments.

For real estate investors, home loans also play a strategic role. Financing allows investors to leverage capital, potentially increasing returns while managing cash flow more efficiently.

Types of Home Loans for Real Estate Financing

Not all home loans are created equal. Choosing the right type of mortgage can significantly impact your total repayment amount and financial flexibility.

Fixed-Rate Home Loans

A fixed-rate home loan offers an interest rate that remains constant throughout the loan term. This option is popular among buyers who value stability and predictable monthly payments. It is especially suitable in a low-interest-rate environment, as borrowers can lock in favorable rates for the long term.

Adjustable-Rate Home Loans

Adjustable-rate mortgages start with a lower interest rate that changes periodically based on market conditions. While initial payments may be lower, rates can increase over time, which may raise monthly installments. This type of loan can work well for buyers who plan to sell or refinance before the adjustment period begins.

Government-Backed Home Loans

In some countries, governments offer special home loan programs to support first-time buyers or low-income households. These loans often come with lower down payment requirements or more flexible qualification standards, making homeownership more accessible.

Key Factors That Affect Home Loan Approval

Understanding what lenders look for can improve your chances of securing favorable real estate financing.

Credit score is one of the most important factors. A strong credit history demonstrates reliability and can help you qualify for lower interest rates. Income stability also plays a major role, as lenders want to ensure borrowers can manage long-term repayments.

Another critical factor is the loan-to-value ratio, which compares the loan amount to the property’s value. A higher down payment usually results in better loan terms and lower risk for the lender.

The Importance of Interest Rates in Home Loans

Interest rates directly influence the total cost of your home loan. Even a small difference in rate can translate into thousands of dollars over the life of the loan. This is why comparing lenders and understanding market trends is essential in real estate financing.

Rates are affected by economic conditions, inflation, and central bank policies. Borrowers who monitor these factors may find better timing opportunities when applying for a mortgage.

Common Mistakes to Avoid When Financing Real Estate

Many buyers focus only on monthly payments without considering the full cost of the loan. Closing fees, insurance, taxes, and maintenance expenses can add up quickly. A realistic budget should include all these elements to avoid financial strain later.

Another common mistake is borrowing the maximum amount offered by the lender. Just because you qualify for a large loan does not mean it aligns with your long-term financial goals. Choosing a comfortable payment level provides more flexibility and peace of mind.

Tips for Choosing the Right Home Loan

Before committing to a mortgage, take time to compare loan offers from different lenders. Look beyond interest rates and review loan terms, penalties, and refinancing options. Transparency and customer service also matter, especially in long-term real estate financing relationships.

Getting pre-approved for a home loan can strengthen your position as a buyer. It shows sellers that you are serious and financially prepared, which can be an advantage in competitive property markets.

Why a Home Loan Guide Matters for Real Estate Success

Real estate financing can feel complex, especially for first-time buyers. Having a solid home loan guide helps simplify the process and reduces costly mistakes. Knowledge empowers buyers to negotiate better terms and make informed decisions that support long-term financial stability.

A well-chosen home loan is not just a way to buy property. It is a strategic tool that can support wealth building, investment growth, and personal security. By understanding the fundamentals of home loans and real estate financing, buyers can approach the market with confidence and clarity.

Choosing the Right Mortgage Path for Your First Home

Choosing the Right Mortgage Path for Your First Home – Buying your first home is one of the biggest financial milestones in life. It is exciting, emotional, and sometimes overwhelming at the same time. Among all the decisions you need to make, choosing the right mortgage path can feel like the most confusing one. The mortgage you choose today will shape your monthly budget, your long-term financial stability, and even how comfortable you feel in your new home.

For first-time buyers, understanding mortgage options is not about mastering complex financial theory. It is about finding a balance between affordability, flexibility, and long-term security. With the right approach, your mortgage can become a helpful tool rather than a financial burden.

Understanding What a Mortgage Really Means

A mortgage is not just a loan. It is a long-term agreement that connects your income, your lifestyle, and your future plans. When you take out a mortgage, you are committing to regular payments over many years, often decades. This makes it essential to look beyond the interest rate and think about the bigger picture.

Many first-time buyers focus only on getting approved, without considering how the loan will feel five or ten years down the road. Will your income grow? Do you plan to start a family? Are you likely to move for work? These questions matter more than most people realize when choosing a mortgage path.

Fixed-Rate vs Adjustable-Rate Mortgages

One of the first choices you will face is between a fixed-rate mortgage and an adjustable-rate mortgage. Each option has its own advantages, depending on your financial comfort level and future expectations.

Fixed-Rate Mortgages for Stability

A fixed-rate mortgage offers consistency. Your interest rate stays the same for the entire loan term, which means your monthly payment remains predictable. For many first-time homeowners, this stability provides peace of mind. You always know what to expect, regardless of changes in the market.

This type of mortgage is often ideal if you plan to stay in your home for a long time or if you prefer a steady, reliable budget. While the initial interest rate may be slightly higher than other options, the long-term predictability can be worth it.

Adjustable-Rate Mortgages for Flexibility

An adjustable-rate mortgage usually starts with a lower interest rate, which can make early payments more affordable. After an initial fixed period, the rate adjusts based on market conditions. This can work well for buyers who expect their income to increase or who plan to sell or refinance before the adjustment period begins.

However, adjustable rates come with uncertainty. Payments can increase over time, and that risk should be carefully considered. For first-time buyers, this option works best when there is a clear plan and enough financial buffer.

How Loan Terms Affect Your Financial Life

The length of your mortgage term plays a major role in how much you pay each month and how much interest you pay overall. Common terms include 15-year and 30-year mortgages, but the right choice depends on your priorities.

A shorter loan term usually means higher monthly payments but lower total interest. This option can help you build equity faster and become debt-free sooner. On the other hand, a longer loan term offers lower monthly payments, giving you more breathing room in your budget.

First-time buyers often choose longer terms to keep payments manageable, especially during the early years of homeownership when expenses tend to add up.

The Importance of Down Payments and Credit Scores

Your down payment and credit score strongly influence the mortgage options available to you. A larger down payment can reduce your loan amount and help you secure better interest rates. It can also eliminate the need for additional insurance costs in some cases.

Credit score matters just as much. Lenders use it to assess risk, and even a small difference in score can lead to significant changes in interest rates. Before applying for a mortgage, it is wise to review your credit report and address any issues you can improve.

Government-Backed Mortgage Options

For many first-time homebuyers, government-backed loans provide a helpful entry point into the housing market. These mortgages are designed to make homeownership more accessible, especially for buyers with limited savings or less-than-perfect credit.

Programs like FHA, VA, and USDA loans offer different benefits, such as lower down payment requirements or more flexible credit guidelines. While these options may include additional conditions, they can open doors that traditional loans may keep closed.

Choosing a Mortgage That Fits Your Lifestyle

The best mortgage is not always the cheapest one on paper. It is the one that fits your lifestyle and financial habits. Some buyers value flexibility and early payoff options, while others prioritize stability and low stress.

Think about how comfortable you are with financial risk, how steady your income is, and how much room you want in your monthly budget. A mortgage should support your life, not limit it.

Planning Beyond the First Year

Many first-time homeowners underestimate how expenses can grow after moving in. Maintenance, repairs, and property taxes can add up quickly. When choosing a mortgage, leave enough room in your budget to handle these costs without strain.

It is also smart to consider refinancing options in the future. Interest rates change, and your financial situation may improve. A mortgage that allows flexibility can give you more options later.

Working With the Right Lender

Choosing the right lender is just as important as choosing the right mortgage product. A good lender will take the time to explain your options clearly and answer your questions honestly. For first-time buyers, guidance and transparency can make a huge difference.

Do not hesitate to compare offers from multiple lenders. Small differences in rates or fees can have a big impact over time. Trust and communication matter as much as numbers.

Final Thoughts on Your First Mortgage Journey

Choosing the right mortgage path for your first home is a personal decision shaped by your goals, finances, and comfort level. There is no universal solution, only the option that works best for you.

By understanding the basics, considering your long-term plans, and staying realistic about your budget, you can move forward with confidence. Your first home should be a source of pride and security, and the right mortgage is a key part of making that happen.

Taking the time to choose wisely today can help ensure that your journey into homeownership starts on solid ground and stays that way for years to come.

Real Estate Financing Tips for Modern Home Buyers

Real Estate Financing Tips for Modern Home Buyers – Buying a home today is very different from what it was ten or even five years ago. Rising property prices, changing mortgage rules, and digital financial tools have reshaped how modern home buyers approach real estate financing. Whether you are a first-time buyer or upgrading to a new property, understanding smart financing strategies can help you secure a better deal and avoid long-term financial stress.

In this guide, we’ll explore practical and realistic real estate financing tips designed specifically for modern home buyers who want to make informed decisions in a competitive housing market.

Understanding the Basics of Real Estate Financing

Before diving into advanced strategies, it’s important to understand what real estate financing actually involves. At its core, real estate financing is the process of securing funds to purchase a property, usually through a mortgage loan. This loan is repaid over time with interest, and the terms you agree to can significantly affect your financial future.

Modern home buyers have more financing options than ever before. Traditional banks, online lenders, credit unions, and even private lenders now compete to offer mortgage products. Each option comes with different interest rates, repayment terms, and qualification requirements. Knowing how these differ can help you choose the right path.

Why Financing Strategy Matters More Than Ever

With property prices climbing in many regions, financing mistakes can be costly. A slightly higher interest rate or poorly structured loan may add tens of thousands of dollars to the total cost of a home. That’s why modern buyers should focus not only on getting approved, but on getting approved under the best possible terms.

Improving Your Financial Profile Before Buying

One of the most effective real estate financing tips is to prepare your financial profile well before you start house hunting. Lenders evaluate several key factors to determine your eligibility and interest rate.

Your credit score plays a major role. A higher score signals lower risk, which often leads to better mortgage rates. Paying bills on time, reducing outstanding debt, and avoiding new credit applications can all help improve your score in the months leading up to your purchase.

Income stability is another critical factor. Lenders prefer borrowers with consistent employment and predictable income. If you’re self-employed or working freelance, maintaining clean financial records and tax filings becomes even more important.

The Importance of Debt-to-Income Ratio

Debt-to-income ratio, or DTI, measures how much of your monthly income goes toward debt payments. A lower DTI improves your chances of mortgage approval and can unlock better loan terms. Modern home buyers often overlook this metric, but reducing existing debt before applying for a mortgage can make a noticeable difference.

Choosing the Right Mortgage Type

Not all mortgages are created equal. Choosing the right type of mortgage is one of the most important real estate financing decisions you’ll make.

Fixed-rate mortgages offer stability, with the same interest rate throughout the loan term. This option is popular among buyers who value predictable monthly payments and long-term planning.

Adjustable-rate mortgages, on the other hand, often start with lower interest rates that change over time. These can be appealing for buyers who plan to sell or refinance within a few years, but they carry more risk if rates rise unexpectedly.

Government-Backed Loan Options

Many modern home buyers qualify for government-backed loans, such as FHA, VA, or USDA loans. These programs often require lower down payments and have more flexible credit requirements. While they may include additional fees or insurance costs, they can be valuable tools for buyers who don’t meet conventional loan standards.

Down Payments and Smart Saving Strategies

Saving for a down payment remains one of the biggest challenges for modern home buyers. While the traditional 20 percent down payment is ideal, many lenders now offer options with lower upfront requirements.

Smaller down payments can make homeownership more accessible, but they may come with trade-offs such as private mortgage insurance or higher interest rates. Understanding these trade-offs is key to making a smart financing decision.

Balancing Down Payment Size and Cash Reserves

Putting all your savings into a down payment may seem like a good idea, but it can leave you financially vulnerable. Maintaining cash reserves for emergencies, repairs, and moving costs is a practical approach that many experienced buyers recommend.

Working With Lenders in the Digital Age

Modern technology has transformed how buyers interact with lenders. Online mortgage platforms allow you to compare rates, submit documents, and track applications with ease. This transparency empowers buyers to shop around and negotiate better terms.

Getting pre-approved before making an offer is especially important in competitive markets. A pre-approval shows sellers that you are a serious buyer and gives you a clear understanding of your budget.

Comparing Offers Beyond Interest Rates

While interest rates matter, they are not the only factor to consider. Closing costs, loan fees, flexibility, and customer service can all impact your experience. Modern home buyers should look at the full picture rather than focusing solely on the advertised rate.

Long-Term Thinking in Real Estate Financing

A home purchase is not just a short-term transaction; it’s a long-term financial commitment. Thinking beyond the first few years can help you avoid regret later on.

Consider how your income, family size, and lifestyle may change over time. Choosing a mortgage that allows for refinancing or early repayment without heavy penalties can provide valuable flexibility.

Refinancing as a Future Opportunity

Interest rates fluctuate, and refinancing can be a powerful tool when rates drop or your financial situation improves. While it’s not guaranteed, keeping refinancing in mind can influence your initial loan choice and help you maximize long-term savings.

Final Thoughts for Modern Home Buyers

Real estate financing doesn’t have to be overwhelming. By understanding the fundamentals, preparing your finances, and choosing the right mortgage strategy, modern home buyers can navigate the process with confidence.

The key is to stay informed, compare options carefully, and think long-term. In today’s evolving housing market, smart financing decisions are just as important as finding the right property. With the right approach, homeownership can be both achievable and financially sustainable.

The Growing Accessibility of Home Equity Loans in Asia

The Growing Accessibility of Home Equity Loans in Asia – Home equity loans are becoming increasingly popular across Asia, driven by rising property ownership, improving financial infrastructure, and changing consumer needs. For many homeowners, property is no longer just a place to live. It has evolved into a valuable financial asset that can unlock liquidity for business, education, investment, or emergency needs.

Across major Asian economies, lenders are simplifying processes, reducing approval times, and expanding access to home-backed credit. This shift is reshaping how individuals and small businesses approach financing, especially in markets where unsecured loans remain expensive or difficult to obtain.

Understanding Home Equity Loans in the Asian Context

A home equity loan allows homeowners to borrow money using their residential property as collateral. The loan amount is usually based on the property’s market value, outstanding mortgage balance, and the borrower’s repayment capacity.

In Asia, this type of financing is often known under different names, including home-backed loans, property-secured credit, or mortgage top-up loans. Regardless of the term, the core concept remains the same: leveraging home value to access more affordable credit.

What makes Asia unique is the diversity of its markets. Developed financial hubs such as Singapore, Hong Kong, Japan, and South Korea offer highly structured home equity products, while emerging markets like Indonesia, Vietnam, Thailand, and the Philippines are rapidly catching up with simplified and more flexible options.

Why Home Equity Loans Are Becoming More Accessible

Rising Property Ownership

Property ownership has grown steadily across Asia over the past two decades. Urbanization, expanding middle-class populations, and government-backed housing programs have all contributed to higher homeownership rates. As more people own homes outright or have built significant equity, lenders see a larger opportunity to offer secured credit.

For banks and financial institutions, home equity loans are relatively lower risk compared to unsecured lending. This has encouraged them to actively promote these products and relax entry barriers.

Improved Financial Infrastructure

Digital banking and fintech adoption have played a major role in increasing accessibility. Property valuations, credit scoring, and document verification are now faster and more transparent than before.

In many Asian countries, loan applications that once took weeks can now be processed in a matter of days. Online submissions, remote property assessments, and automated underwriting systems have reduced friction for both lenders and borrowers.

Competitive Lending Markets

Competition among banks, non-bank financial institutions, and fintech lenders has pushed interest rates down and terms to become more borrower-friendly. Flexible repayment tenures, higher loan-to-value ratios, and customized loan structures are now common.

This competitive environment benefits homeowners who are seeking better financing options without excessive paperwork or rigid requirements.

Key Benefits of Home Equity Loans in Asia

One of the main reasons homeowners choose home equity loans is cost efficiency. Interest rates are generally lower than personal loans or credit cards because the loan is secured by property.

Another advantage is loan size. Home equity loans often provide access to larger amounts of capital, making them suitable for business expansion, property renovation, education funding, or debt consolidation.

In many Asian markets, borrowers also enjoy longer repayment periods, which helps keep monthly installments manageable. This makes home-backed credit a practical solution for long-term financial planning.

Popular Uses of Home Equity Loans

Business and Entrepreneurship

Small and medium-sized enterprises are the backbone of many Asian economies. Home equity loans are frequently used by entrepreneurs to fund startups, expand operations, or manage cash flow.

For business owners who may struggle to qualify for traditional business loans, using residential property as collateral provides an alternative path to financing.

Education and Family Needs

Education costs continue to rise across Asia, especially for overseas study or private institutions. Home equity loans offer a structured and affordable way for families to invest in education without relying on high-interest unsecured loans.

Healthcare expenses and family emergencies are also common reasons homeowners tap into their property equity.

Property Investment and Renovation

Many borrowers use home equity loans to renovate existing properties or invest in additional real estate. In markets where property values are appreciating, this strategy allows homeowners to maximize asset utilization while maintaining ownership.

Regional Trends Across Asia

In East Asia, countries like Japan and South Korea have mature mortgage markets with stable home equity loan offerings. Borrowers benefit from low interest rates and strong consumer protection frameworks.

Southeast Asia is experiencing rapid growth in home-backed lending. Indonesia, Thailand, and Vietnam have seen increasing demand as financial literacy improves and lenders introduce simplified loan products tailored to local income structures.

In South Asia, particularly India, home equity loans are gaining traction as an alternative to business and personal loans. Banks and housing finance companies actively market these products to salaried professionals and self-employed individuals.

Risks and Considerations for Borrowers

While accessibility is improving, borrowers should remain aware of the risks. A home equity loan places the property at risk if repayments are not met. Responsible borrowing and realistic repayment planning are essential.

Interest rates, while lower than unsecured credit, may be variable depending on the lender and market conditions. Borrowers should also consider fees related to appraisal, legal documentation, and early repayment.

Understanding local regulations and lender terms is critical, especially in markets where consumer protection standards vary.

The Future of Home Equity Lending in Asia

The outlook for home equity loans in Asia remains positive. As property markets mature and digital lending continues to expand, accessibility is expected to improve further.

Fintech innovation is likely to introduce more personalized loan offerings, faster approvals, and greater transparency. At the same time, regulators across Asia are strengthening frameworks to ensure responsible lending and borrower protection.

For homeowners, this means greater opportunity to turn property value into practical financial leverage. For lenders, it represents a stable and scalable credit segment with long-term growth potential.

Final Thoughts

The growing accessibility of home equity loans in Asia reflects broader changes in how people view property ownership and financial planning. Homes are no longer static assets but dynamic tools that can support personal goals, business ambitions, and long-term stability.

As awareness increases and lending processes become more streamlined, home equity loans are set to play an even bigger role in Asia’s evolving financial landscape. For the right borrower, used wisely, they offer a powerful and flexible financing solution grounded in one of the region’s most valuable assets: real estate.

Understanding Property Installments Without Confusion

Understanding Property Installments Without Confusion – Buying property is often described as one of the biggest financial decisions in life. For many people, paying the full price upfront is simply not realistic. This is where property installments come into play. Unfortunately, the concept of property installments can feel confusing, especially for first-time buyers who are not familiar with financial terms or real estate processes.

Understanding how property installments work does not have to be complicated. With the right perspective and clear explanation, you can make smarter decisions and avoid costly mistakes. This article breaks down the idea of property installments in a simple and practical way, so you can move forward with confidence.

What Are Property Installments?

Property installments refer to a payment system where a buyer pays for a property in stages rather than all at once. Instead of handing over a large sum, payments are spread over a specific period, usually monthly or yearly, depending on the agreement.

This system allows buyers to own or secure a property while managing their cash flow more comfortably. Property installments are commonly used for houses, apartments, land, and even commercial buildings.

At its core, the installment system is about flexibility. It opens the door to property ownership for people who have stable income but limited savings.

How Property Installments Actually Work

When you buy a property using installments, the total price is divided into smaller payments. These payments are made over a fixed duration, which can range from a few years to several decades.

The structure usually starts with a down payment. This is an initial amount paid upfront to secure the property. After that, the remaining balance is paid in installments according to the agreed schedule.

In many cases, installments include interest, especially when financing is provided by a bank or financial institution. However, some developers offer installment plans without bank involvement, which can reduce complexity but may come with different terms.

Bank-Based Installments

Bank-based property installments involve a mortgage or home loan. The bank pays the developer or seller, and the buyer repays the bank over time. Interest rates, loan tenure, and approval requirements play a big role in this type of installment.

This option is popular because it allows longer repayment periods and often offers legal protection through regulated systems.

Developer Installment Plans

Developer installment plans are agreements directly between the buyer and the property developer. These plans may offer shorter repayment periods and sometimes lower upfront requirements.

While they can be attractive, buyers should carefully review contracts to understand penalties, ownership status, and payment deadlines.

Why Property Installments Are So Popular

Property installments have become increasingly popular for several reasons. Rising property prices make it harder to pay in cash, especially in urban areas. Installments provide a practical solution that aligns with modern income patterns.

Another reason is accessibility. Installment plans allow younger buyers, entrepreneurs, and families to invest in property earlier rather than waiting years to save enough money.

Installments also help with financial planning. Fixed monthly payments make budgeting easier and reduce the pressure of large, sudden expenses.

Common Misunderstandings About Property Installments

Many people avoid property installments because of misconceptions. One common belief is that installments are always risky or expensive. In reality, the risk depends on the terms, not the concept itself.

Another misunderstanding is assuming that all installment plans are the same. Each property, developer, or bank can offer very different conditions. Interest rates, payment schedules, and penalties can vary widely.

Some buyers also believe that missing one payment automatically results in losing the property. While late payments can cause problems, most agreements include grace periods or restructuring options.

Key Things to Check Before Choosing an Installment Plan

Before committing to a property installment plan, it is essential to read and understand the agreement. Look closely at the total price you will pay by the end of the installment period, not just the monthly amount.

Make sure you understand how interest is calculated and whether it is fixed or variable. Small differences in interest rates can significantly impact long-term costs.

It is also important to check ownership status. Some installment plans transfer ownership only after full payment, while others offer conditional ownership earlier.

Managing Property Installments Without Stress

Managing property installments successfully comes down to preparation and discipline. Choose a payment plan that fits your income, not just your expectations. It is better to select a slightly longer tenure than to struggle with high monthly payments.

Setting aside an emergency fund can help protect you if unexpected expenses arise. This ensures you can continue paying installments even during difficult times.

Regularly reviewing your finances and communicating with lenders or developers can also prevent small issues from becoming serious problems.

The Role of Financial Planning

Good financial planning makes property installments much easier to handle. Knowing your monthly expenses, income stability, and future goals helps you choose a realistic plan.

Avoid stretching your budget to the limit. Property ownership should improve your quality of life, not create constant financial pressure.

Property Installments as a Long-Term Investment

Beyond personal use, property installments are often used as an investment strategy. Investors use installment plans to acquire assets while preserving cash for other opportunities.

Over time, property values may increase, allowing investors to benefit from appreciation while paying installments gradually. Rental income can also help cover monthly payments.

However, investment-focused buyers should carefully analyze market conditions, location potential, and long-term demand before committing.

Final Thoughts on Understanding Property Installments

Property installments are not something to fear. They are simply a financial tool designed to make property ownership more accessible. When understood correctly, they offer flexibility, opportunity, and long-term value.

The key is clarity. By understanding how installments work, what to look for in agreements, and how to manage payments responsibly, buyers can avoid confusion and make informed decisions.

Whether you are buying your first home or expanding your property portfolio, taking the time to understand property installments can save you money, reduce stress, and lead to smarter investments in the future.

Why Buying a House with Cash Is Cheaper Than Financing

Why Buying a House with Cash Is Cheaper Than Financing – Buying a home is one of the biggest financial decisions most people make in their lifetime. While mortgages and financing are common paths to homeownership, paying with cash offers unique advantages that are often overlooked. Although it requires significant upfront funds, buying a house with cash can actually be cheaper in the long run compared to taking out a loan.

This article explores why cash purchases can save money, reduce stress, and create opportunities that financing may not offer.

Understanding the Cost of Financing a Home

When most people think about buying a house, a mortgage is usually the default option. Mortgages allow buyers to spread the cost of a home over many years, making high-priced properties more accessible. However, this convenience comes with added costs that can significantly increase the total price of a home.

Interest rates, loan origination fees, mortgage insurance, and other charges are part of the financing process. Even with a relatively low interest rate, the cumulative cost of paying a mortgage over 15 or 30 years can be substantial. For example, a 30-year loan at a 6% interest rate can add hundreds of thousands of dollars in interest to the cost of a home. This extra expense is avoided entirely when paying cash.

The Hidden Expenses of Mortgages

It’s not just interest that makes financing expensive. Lenders often require appraisal fees, underwriting fees, and closing costs, which can quickly add up. Some loans also require private mortgage insurance, especially if the buyer cannot provide a large down payment. Over time, these fees create a noticeable gap between the sticker price of a home and what a financed buyer actually pays.

Cash buyers, on the other hand, bypass these costs entirely. Without lenders involved, closing is often simpler and faster, with fewer fees to pay upfront.

Immediate Financial Benefits of Paying Cash