Will Home Loan Interest Rates Decrease in Indonesia banks 2026

Will Home Loan Interest Rates Decrease in Indonesia banks 2026 | Buying a home is one of the biggest financial decisions most people will ever make. For many Indonesians, purchasing property depends heavily on obtaining a home loan, making interest rates a key factor in determining affordability.

Throughout 2026, many prospective buyers have been asking the same question: Will home loan interest rates decrease at Indonesian banks? The answer isn’t as straightforward as many hope. Mortgage rates are influenced by a combination of Bank Indonesia’s monetary policy, inflation, competition among banks, economic growth, and the broader financial market.

While some banks continue to offer attractive promotional fixed-rate mortgages, overall borrowing costs remain closely tied to the country’s interest-rate environment. Understanding these factors can help buyers decide whether to purchase a home now or wait for potentially lower financing costs.

This article explains what affects home loan interest rates in Indonesia, what borrowers can expect in 2026, and how to prepare for the best mortgage opportunities.

What Determines Home Loan Interest Rates?

Mortgage interest rates do not change randomly.

Banks calculate lending rates based on several economic indicators that influence both borrowing costs and financial risk.

The most important factors include:

- Bank Indonesia’s benchmark interest rate.

- Inflation.

- Economic growth.

- Liquidity in the banking sector.

- Competition among lenders.

- Credit risk.

- Property market conditions.

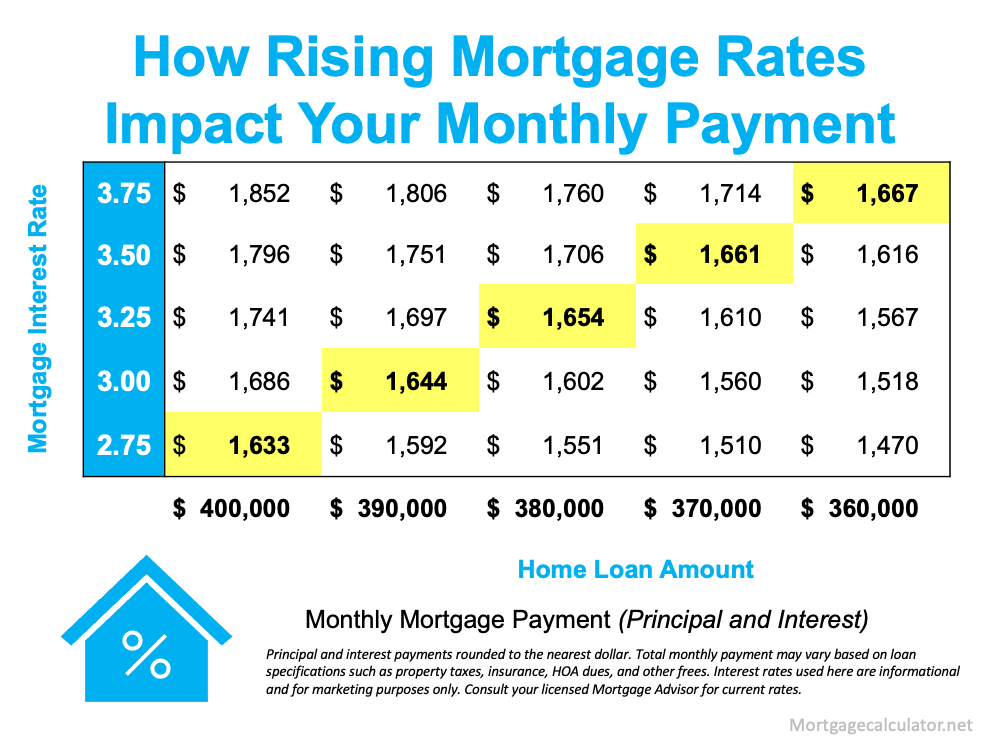

When borrowing costs increase for banks, mortgage rates often rise as well. Conversely, a lower-rate environment can create opportunities for banks to introduce more competitive home loan products.

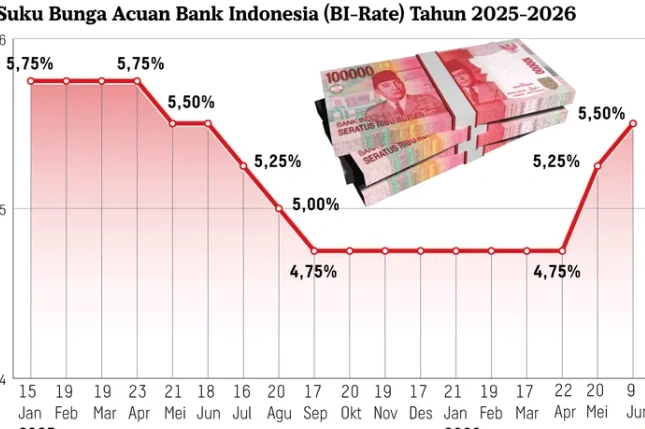

The Role of Bank Indonesia

Bank Indonesia plays a major role in influencing mortgage rates through its benchmark policy rate.

When the central bank raises interest rates to control inflation or stabilize the rupiah, banks generally face higher funding costs. Those increases can eventually affect mortgage pricing, particularly for floating-rate home loans.

In 2026, Bank Indonesia has adjusted its policy stance in response to inflationary pressures and currency stability, meaning expectations for significantly lower mortgage rates have become more cautious.

Are Mortgage Rates Likely to Fall in 2026?

The possibility of lower mortgage rates depends on several economic developments.

If inflation remains under control and financial markets stabilize, banks could become more competitive by offering lower promotional fixed rates or special financing packages.

However, if inflation remains elevated or the central bank maintains tighter monetary policy, widespread reductions in mortgage interest rates may be limited.

Rather than expecting dramatic decreases across the industry, borrowers are more likely to see selective promotional offers from individual banks than a sharp nationwide decline in lending rates.

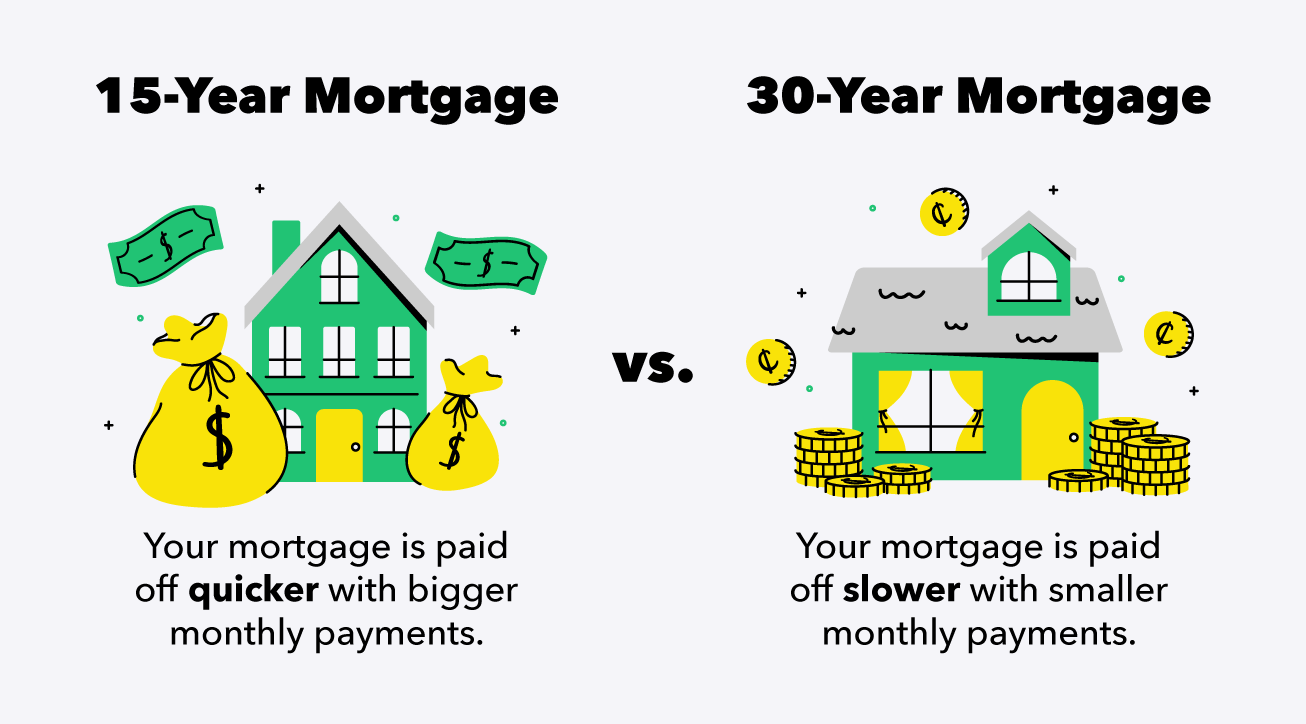

Fixed-Rate vs. Floating-Rate Mortgages

Understanding the difference between fixed and floating interest rates is essential before applying for a mortgage.

Fixed-Rate Mortgage

A fixed-rate mortgage keeps the interest rate unchanged during the promotional period.

Advantages include:

- Predictable monthly payments.

- Easier financial planning.

- Protection from rising interest rates.

Many Indonesian banks offer fixed-rate promotions during the first few years of the loan.

Floating-Rate Mortgage

After the promotional period ends, many mortgages transition to a floating rate.

Floating rates can:

- Increase when benchmark rates rise.

- Decrease if market conditions improve.

- Change periodically according to bank policies.

Borrowers should carefully understand when their loan changes from fixed to floating rates before signing a mortgage agreement.

Why Banks Continue Offering Promotional Rates

Even during periods of higher benchmark interest rates, banks continue competing for mortgage customers.

Common promotional offers include:

- Low introductory fixed rates.

- Reduced administrative fees.

- Lower appraisal costs.

- Cashback programs.

- Flexible repayment options.

- Partnership discounts with property developers.

These promotions can significantly reduce borrowing costs during the early years of home ownership, even if floating rates remain higher later.

Is 2026 Still a Good Time to Buy a Home?

For many buyers, waiting for significantly lower interest rates may not always be the best strategy.

Several factors should be considered:

- Current property prices.

- Personal financial readiness.

- Job stability.

- Down payment availability.

- Monthly repayment affordability.

- Long-term housing goals.

If the right property is available and monthly payments comfortably fit your budget, delaying a purchase solely in anticipation of lower interest rates may not necessarily produce better overall financial outcomes.

Tips for Getting the Best Mortgage Rate

Before applying for a home loan, borrowers can improve their chances of receiving competitive financing by following several practical steps.

Compare Multiple Banks

Interest rates, promotional periods, and fees can vary significantly between lenders.

Comparing several mortgage products helps identify the most suitable financing option.

Maintain a Strong Credit Profile

Banks evaluate applicants based on their repayment history and financial stability.

A healthy credit record often improves eligibility for better interest rates.

Prepare a Larger Down Payment

Higher down payments reduce lending risk for banks and may improve financing terms.

Understand the Total Cost

The advertised interest rate is only one part of the mortgage.

Borrowers should also review:

- Administrative fees.

- Insurance costs.

- Appraisal fees.

- Early repayment charges.

- Floating-rate conditions.

Understanding the complete financing package prevents unexpected expenses later.

What First-Time Homebuyers Should Know

For first-time buyers, choosing the right mortgage involves more than finding the lowest advertised rate.

Important considerations include:

- Loan tenure.

- Monthly affordability.

- Emergency savings.

- Future income growth.

- Lifestyle changes.

- Long-term financial goals.

Buying a home should strengthen financial security rather than create unnecessary financial pressure.

Frequently Asked Questions

Will Indonesian mortgage rates definitely decrease in 2026?

Not necessarily. Future mortgage rates depend on inflation, Bank Indonesia’s monetary policy, banking competition, and overall economic conditions.

Should I wait for lower mortgage rates?

Waiting may benefit some buyers, but property prices and personal financial circumstances are equally important factors when deciding to purchase a home.

Are promotional mortgage rates worth considering?

Yes. Many banks offer attractive fixed-rate promotions during the first years of a mortgage, which can reduce initial monthly payments.

What affects floating mortgage rates?

Floating rates generally follow changes in market conditions, benchmark interest rates, and each bank’s lending policies.

How can I qualify for better mortgage rates?

Maintaining good credit, preparing a larger down payment, comparing several banks, and demonstrating stable income can improve your chances of securing competitive financing.

Whether home loan interest rates decrease in 2026 will largely depend on Indonesia’s economic outlook, inflation, and future decisions by Bank Indonesia. While some lenders may introduce competitive promotional mortgage packages, borrowers should not expect a dramatic decline in mortgage rates across the entire banking industry in the near term.

Instead of focusing solely on interest-rate forecasts, prospective homeowners should evaluate their financial readiness, compare mortgage products carefully, and choose a loan that fits their long-term budget. A competitive mortgage is not simply the one with the lowest advertised rate—it is the one that balances affordability, flexibility, and overall borrowing costs.

For many Indonesians, buying a home in 2026 can still be a smart financial decision, provided it is supported by careful planning and informed borrowing choices.