How to Apply for a Home Loan as a Self-Employed Borrower

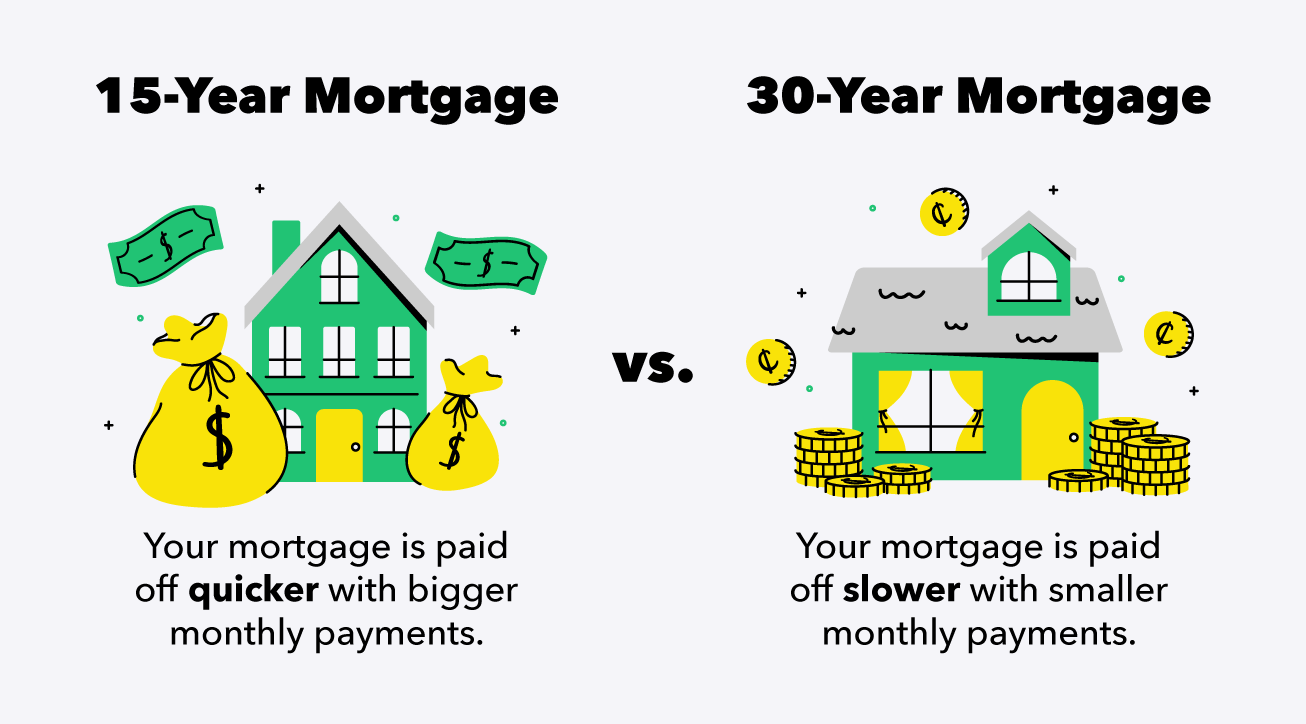

Should You Consider a 15-Year vs. 30-Year Home Loan?

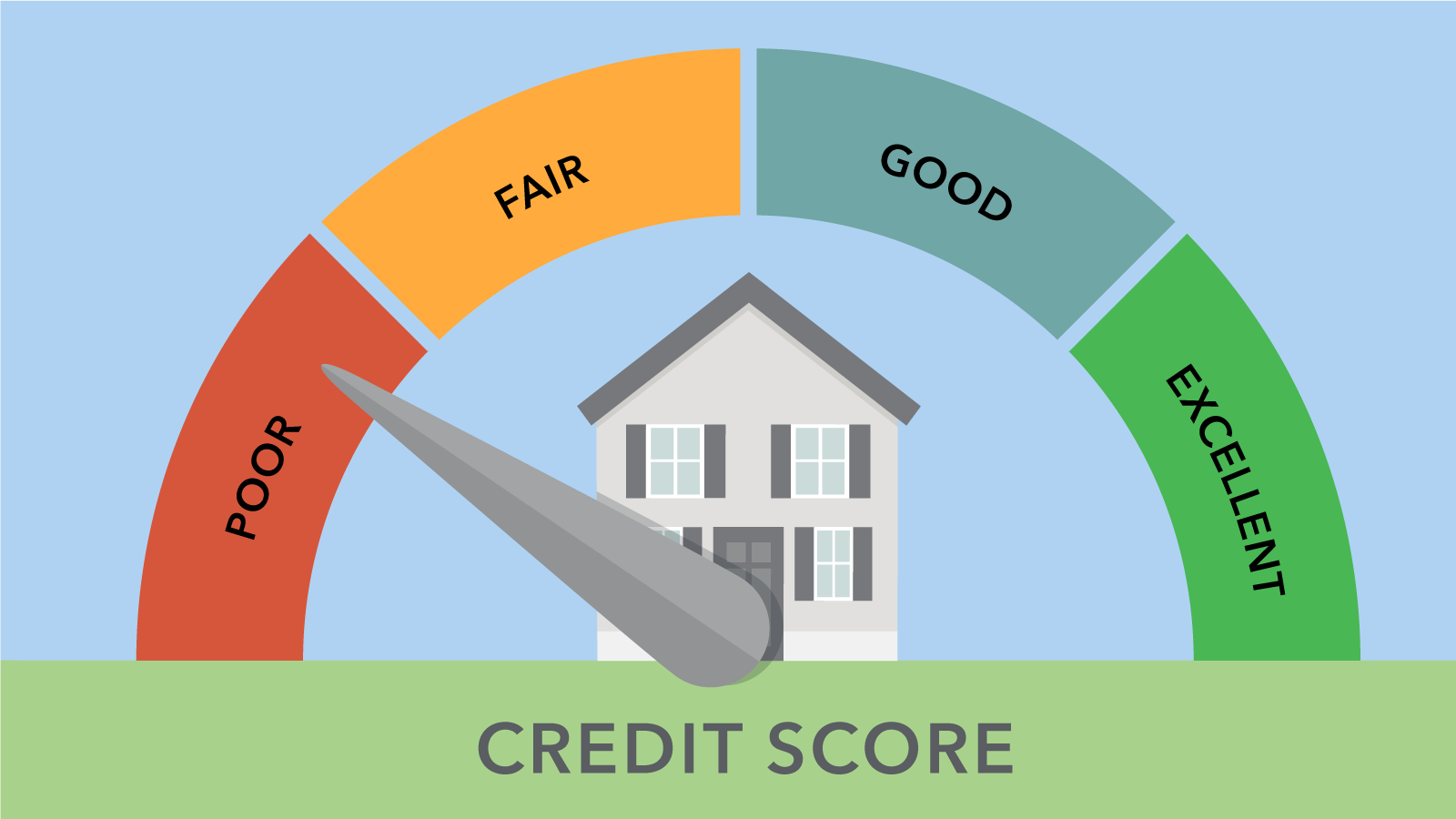

How to Secure a Home Loan With a Low Credit Score

How to Secure a Home Loan With a Low Credit Score – Buying a home is a big milestone, but if your credit score is less than ideal, the process can feel overwhelming. Many people assume that a low credit score automatically disqualifies them from getting a mortgage. The truth is, that’s not always the case. There are still ways to secure a home loan with a low credit score, as long as you understand your options and prepare strategically.

Lenders look at more than just your credit score. While your score plays an important role in determining your eligibility and interest rate, it is only one part of the overall picture. Income stability, debt-to-income ratio, employment history, and the size of your down payment also matter. If you approach the process wisely, you can increase your chances of approval even with less-than-perfect credit.

Understanding How Credit Score Affects Your Mortgage

Your credit score is a numerical representation of your creditworthiness. It tells lenders how reliable you have been in repaying debts. Most conventional lenders prefer borrowers with scores above 620, but this does not mean lower scores are automatically rejected.

For example, loans backed by the Federal Housing Administration are designed to help borrowers with lower credit scores. FHA loans often allow credit scores as low as 580, and sometimes even lower with a larger down payment. This makes them a popular option for first-time homebuyers who may not have strong credit histories.

On the other hand, conventional loans typically follow guidelines set by Fannie Mae and Freddie Mac. These institutions usually require higher credit scores and stricter financial qualifications. However, each lender has its own criteria, so shopping around is essential.

A lower credit score generally means higher interest rates. This is because lenders see you as a higher risk. Over the life of a mortgage, even a small difference in interest rate can significantly affect how much you pay. That’s why it’s important to explore strategies that can improve your application strength before applying.

Practical Steps to Secure a Home Loan With a Low Credit Score

Getting approved for a mortgage with a low credit score is possible if you take the right steps. Preparation and planning can make a huge difference in how lenders view your application.

Review and Improve Your Credit Before Applying

Before you start applying for a home loan, check your credit report carefully. Look for errors such as incorrect late payments, duplicate accounts, or debts that have already been paid. Disputing inaccuracies can sometimes boost your score faster than you expect.

If possible, spend a few months improving your credit. Pay all bills on time, reduce credit card balances, and avoid opening new lines of credit. Even a small increase in your score can qualify you for better mortgage terms.

Consistency matters more than quick fixes. Lenders want to see stable financial behavior. Showing several months of on-time payments can strengthen your case, even if your score is still below average.

Save for a Larger Down Payment

One of the most effective ways to secure a home loan with a low credit score is by offering a larger down payment. A higher down payment reduces the lender’s risk because you are borrowing less money. It also demonstrates financial responsibility.

If you can put down 10% to 20% instead of the minimum requirement, lenders may be more willing to work with you. In some cases, a larger down payment can even offset the impact of a lower credit score when determining your interest rate.

Saving more upfront also reduces your monthly mortgage payments and may help you avoid private mortgage insurance, depending on the loan type.

Lower Your Debt-to-Income Ratio

Your debt-to-income ratio, often called DTI, measures how much of your monthly income goes toward paying debts. Lenders use this ratio to evaluate whether you can afford a mortgage payment.

If you have a low credit score, lowering your DTI can strengthen your application. Focus on paying off smaller debts such as credit cards or personal loans. Avoid taking on new debt before applying for a home loan.

A lower DTI shows lenders that you are not financially overextended. This can increase your chances of getting approved even if your credit score is less than ideal.

Exploring Loan Options for Low Credit Borrowers

Not all mortgage products are created equal. Some are specifically designed to help borrowers with lower credit scores achieve homeownership.

FHA loans, backed by the Federal Housing Administration, are among the most popular options. They offer more flexible credit requirements and lower down payment options compared to conventional loans. However, they do require mortgage insurance premiums, which add to the overall cost.

Another potential option is a VA loan, guaranteed by the U.S. Department of Veterans Affairs. These loans are available to eligible veterans, active-duty service members, and certain military spouses. VA loans often have no minimum credit score requirement set by the agency, though individual lenders may impose their own standards.

USDA loans, supported by the U.S. Department of Agriculture, are designed for rural and suburban homebuyers who meet income requirements. These loans can offer low interest rates and zero down payment options, making them attractive to borrowers with moderate or lower credit scores.

Each program has specific eligibility requirements, so it’s important to research which one fits your financial situation and long-term goals.

Work With the Right Lender

When trying to secure a home loan with a low credit score, choosing the right lender can make a significant difference. Some lenders specialize in working with borrowers who have less-than-perfect credit. They may offer more flexible underwriting standards or provide guidance on improving your application before submission.

It’s wise to compare multiple lenders and request pre-approval quotes. This allows you to see potential interest rates and loan terms without committing immediately. Make sure to ask about all associated costs, including closing fees and mortgage insurance.

Building a relationship with a knowledgeable loan officer can also help. An experienced professional can suggest specific actions to improve your approval chances and recommend loan programs suited to your profile.

Consider a Co-Signer or Alternative Strategies

If your credit score is too low to qualify on your own, adding a co-signer with stronger credit may help. A co-signer agrees to share responsibility for the loan, which reduces the lender’s risk.

However, this is a serious commitment. If you fail to make payments, your co-signer’s credit will also be affected. Make sure both parties fully understand the responsibilities involved before moving forward.

Another strategy is to delay your home purchase and focus on rebuilding your credit. While this requires patience, it can save you thousands of dollars in interest over the life of the loan.

Final Thoughts on Securing a Home Loan With a Low Credit Score

Securing a home loan with a low credit score is not impossible. It requires preparation, realistic expectations, and a willingness to explore alternative mortgage options. By improving your credit habits, saving for a larger down payment, lowering your debt-to-income ratio, and choosing the right loan program, you can significantly increase your chances of approval.

How to Use a Home Loan Calculator to Estimate Your Payments

How to Use a Home Loan Calculator to Estimate Your Payments – Buying a home is an exciting milestone, but understanding the financial commitment can sometimes feel overwhelming. One of the easiest ways to get a clearer picture of your potential mortgage is by using a home loan calculator. These tools provide an estimate of your monthly payments, helping you plan your budget and make informed decisions. By knowing what to expect, you can approach the home-buying process with confidence and clarity.

What is a Home Loan Calculator?

A home loan calculator is an online tool that estimates your monthly mortgage payments based on factors such as loan amount, interest rate, loan term, and down payment. It can also factor in additional costs like property taxes and homeowners insurance, giving you a comprehensive view of what your monthly obligations might look like. While it doesn’t replace professional financial advice, a calculator provides a helpful starting point for planning and budgeting.

Using a calculator allows you to test different scenarios. For example, you can see how increasing your down payment, reducing your loan term, or adjusting the interest rate affects your monthly payments. This flexibility is invaluable when comparing loan options and understanding how small changes can make a big difference over time.

Why Using a Home Loan Calculator Matters

Understanding your potential mortgage payments is essential for making informed financial decisions. A calculator helps you avoid overextending yourself and ensures you choose a loan that fits your budget. It also allows you to plan for related expenses, such as property taxes, insurance, and maintenance, so there are no surprises once you move in.

Additionally, using a calculator can strengthen your position when negotiating with lenders. By knowing how different terms affect your monthly payments, you can confidently discuss rates, repayment options, and loan terms. It helps you approach the process strategically rather than relying solely on the lender’s guidance.

How to Use a Home Loan Calculator

Using a home loan calculator is straightforward, but it’s important to input accurate information to get reliable estimates. Here’s a step-by-step guide to using one effectively.

Step 1: Enter the Loan Amount

The loan amount is the total money you plan to borrow from the lender. It is usually the price of the property minus your down payment. For example, if the home costs $300,000 and you are putting down $60,000, your loan amount would be $240,000. Accurately entering this figure ensures the calculator provides a realistic estimate of your monthly payments.

Step 2: Input the Interest Rate

The interest rate is a key factor in determining your monthly payments. Even a small difference in rates can have a significant impact over the life of the loan. Be sure to use the current rate offered by your lender or a rate you are likely to qualify for based on your credit profile. Many calculators allow you to test different interest rates to see how they affect your payments.

Step 3: Choose the Loan Term

The loan term is the length of time you have to repay the mortgage, typically 15, 20, or 30 years. Shorter terms usually mean higher monthly payments but less interest paid over time, while longer terms reduce monthly payments but increase total interest. By adjusting the loan term in the calculator, you can find a balance between affordable monthly payments and minimizing total interest.

Step 4: Include Additional Costs

Some home loan calculators allow you to include property taxes, homeowners insurance, and mortgage insurance. These costs can significantly impact your monthly payments, so including them provides a more realistic estimate. Even if your calculator does not have this option, be sure to account for these expenses separately when planning your budget.

Step 5: Review and Adjust

Once you enter all the details, the calculator will provide an estimate of your monthly payment. Take time to review the result and experiment with different scenarios. For instance, increasing your down payment or slightly adjusting the interest rate can lower your payments. Testing different options helps you understand the flexibility you have and identify the most manageable mortgage for your situation.

Benefits of Using a Home Loan Calculator

Home loan calculators offer several advantages for prospective borrowers. They simplify complex calculations, allowing you to focus on other aspects of the home-buying process. They also help you:

-

Plan your budget accurately. Knowing your estimated monthly payments prevents overspending.

-

Compare loan options. Calculators allow you to see how different rates, terms, and down payments affect payments.

-

Negotiate with lenders. Being informed gives you leverage when discussing loan terms.

-

Reduce stress. Understanding your potential financial commitment makes the home-buying process less overwhelming.

By providing clarity and insight, calculators empower you to make decisions with confidence rather than relying on guesswork.

Tips for Maximizing Accuracy

While home loan calculators are useful, accuracy depends on the information you provide. Here are a few tips to get the most out of these tools:

-

Use realistic numbers. Base your inputs on actual quotes from lenders rather than estimates.

-

Factor in all costs. Don’t forget taxes, insurance, and potential maintenance expenses.

-

Check multiple calculators. Different calculators may use slightly different formulas, so comparing results can give you a more accurate range.

-

Update numbers regularly. Interest rates, property prices, and personal finances change over time, so recalculate if any key variables change.

When to Use a Home Loan Calculator

A home loan calculator is helpful at multiple stages of the home-buying process. Initially, it helps you set a budget and determine what price range you can afford. Later, it allows you to compare different loan offers and see how varying interest rates or terms affect your payments. Even after securing a mortgage, it can help you plan for refinancing options or paying off your loan faster.

Using a calculator early and often ensures you make informed decisions every step of the way. It’s a simple tool that can prevent costly mistakes and make your financial planning more precise.

Final Thoughts: Empower Your Home-Buying Decisions

Estimating your home loan payments is a crucial step in achieving a successful and stress-free home purchase. A home loan calculator provides a clear view of your potential monthly payments, helping you budget, compare loan options, and negotiate effectively with lenders. By entering accurate information and testing different scenarios, you can gain confidence in your decisions and choose a mortgage that aligns with your financial goals.

Whether you are a first-time homebuyer or an experienced investor, taking the time to use a home loan calculator ensures that you understand the full scope of your financial commitment. It’s a small step that can have a big impact on your long-term financial well-being, turning what might feel like a complicated process into an empowering and manageable experience.

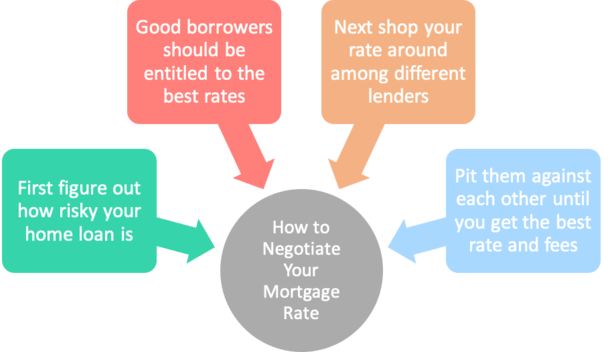

How to Negotiate Your Home Loan Terms With Lenders

How to Negotiate Your Home Loan Terms With Lenders – Buying a home is one of the biggest financial decisions most people will make in their lifetime. While finding the perfect property is exciting, negotiating the terms of your home loan is equally important. Many borrowers accept the first loan offer they receive, but understanding how to negotiate with lenders can save you thousands of dollars over the life of the mortgage. With the right approach, preparation, and knowledge, you can secure favorable interest rates, lower fees, and flexible repayment options that suit your financial goals.

Why Negotiating Your Home Loan Matters

A home loan is a long-term commitment, often lasting 15 to 30 years. Even a small reduction in interest rates or fees can make a significant difference in your monthly payments and total interest paid. Negotiating your loan terms allows you to gain control over costs, reduce financial stress, and customize your mortgage to fit your needs. Lenders often have some flexibility, especially for borrowers with strong credit scores, stable income, and a clear understanding of the market. Knowing your leverage and approaching the conversation strategically can put you in a strong position.

Understand Your Financial Position

Before entering negotiations, it’s essential to have a clear picture of your financial situation. Lenders will consider your credit score, income, debt-to-income ratio, and employment stability when determining the terms of your loan. By reviewing your finances in advance, you can identify areas that may improve your negotiation power. For instance, paying down high-interest debts or correcting errors on your credit report can boost your creditworthiness. Understanding your finances also helps you determine the type of mortgage you can realistically afford and the monthly payments that fit your budget.

Check Your Credit Score

Your credit score is one of the most critical factors in home loan negotiations. Lenders use it to assess risk and decide on interest rates. A higher credit score often translates into lower rates and more favorable terms. Before negotiating, check your credit report for inaccuracies, pay down outstanding balances, and avoid taking on new loans. Demonstrating financial responsibility can increase a lender’s willingness to offer better terms.

Compare Loan Offers

Not all lenders offer the same rates or conditions, so shopping around is a key step in negotiation. Comparing multiple loan offers gives you leverage when discussing terms with your preferred lender. By showing that you have options, you signal that you are an informed borrower and can walk away if terms are not favorable. Pay attention to interest rates, origination fees, closing costs, and repayment flexibility when evaluating offers. Even small differences in rates can save you significant amounts over the life of your mortgage.

Consider Different Loan Types

Lenders provide a variety of loan options, including fixed-rate, adjustable-rate, and interest-only mortgages. Each type comes with different benefits and risks. Understanding the options allows you to negotiate terms that align with your long-term financial goals. For example, a fixed-rate mortgage offers predictable monthly payments, while an adjustable-rate mortgage may provide lower initial rates but can fluctuate over time. Being informed about these differences strengthens your position in discussions with lenders.

Be Prepared to Ask

Negotiation is not just about waiting for the lender to offer better terms—it involves proactive questions. Ask about interest rate reductions, lower origination fees, or the possibility of waiving certain closing costs. Some lenders may also offer flexible repayment schedules or discounts for automatic payments. By initiating the conversation, you demonstrate that you are an engaged borrower who understands the value of the loan. Lenders may be more willing to accommodate requests when they see that you are serious, organized, and financially responsible.

Leverage Your Strengths

Your financial profile can serve as a powerful tool in negotiation. Stable income, a high credit score, a sizable down payment, or a long-standing relationship with a bank can all be used to your advantage. Highlight these strengths during discussions with your lender. For example, offering a larger down payment might encourage the lender to lower your interest rate, as it reduces their risk. Demonstrating reliability and preparedness can make lenders more flexible in offering favorable terms.

Understand Lender Incentives

Lenders often have incentives to attract borrowers, such as reduced fees for refinancing, special rates for certain customer groups, or promotions for first-time homebuyers. By researching these incentives, you can identify opportunities to negotiate. Understanding what motivates a lender helps you frame your requests in a way that aligns with their goals. This approach can increase the likelihood of achieving better terms without pushing too hard or risking the relationship.

Don’t Rush the Process

Negotiating a home loan is not something to be rushed. Take the time to review offers, ask questions, and understand the implications of different terms. Rushing may lead to missing hidden fees, unfavorable conditions, or long-term costs. Patience allows you to weigh your options carefully and enter discussions with confidence. A well-considered approach shows lenders that you are informed and serious, which can make them more willing to negotiate.

Seek Professional Advice

If you’re unsure about the negotiation process, consider consulting a mortgage broker or financial advisor. Professionals can provide insights into market trends, lender practices, and optimal strategies for negotiation. Their expertise can help you navigate complex loan documents and identify opportunities that might not be immediately apparent. While professional advice may come at a cost, the potential savings from securing better loan terms often outweigh the expense.

Final Thoughts: Negotiation is Key to Savings

Negotiating your home loan terms is an essential step in responsible homeownership. By understanding your financial position, comparing offers, asking informed questions, and leveraging your strengths, you can secure a mortgage that works for you. Lenders have flexibility, and informed borrowers who take the time to negotiate often enjoy lower rates, reduced fees, and more favorable conditions.

Remember, a home loan is a long-term commitment, and every dollar saved in interest or fees matters. Approaching negotiations strategically not only reduces financial strain but also empowers you to make decisions that align with your long-term goals. With preparation, knowledge, and confidence, you can turn the home loan process into an opportunity to gain financial advantage rather than simply a necessary step in buying a property.

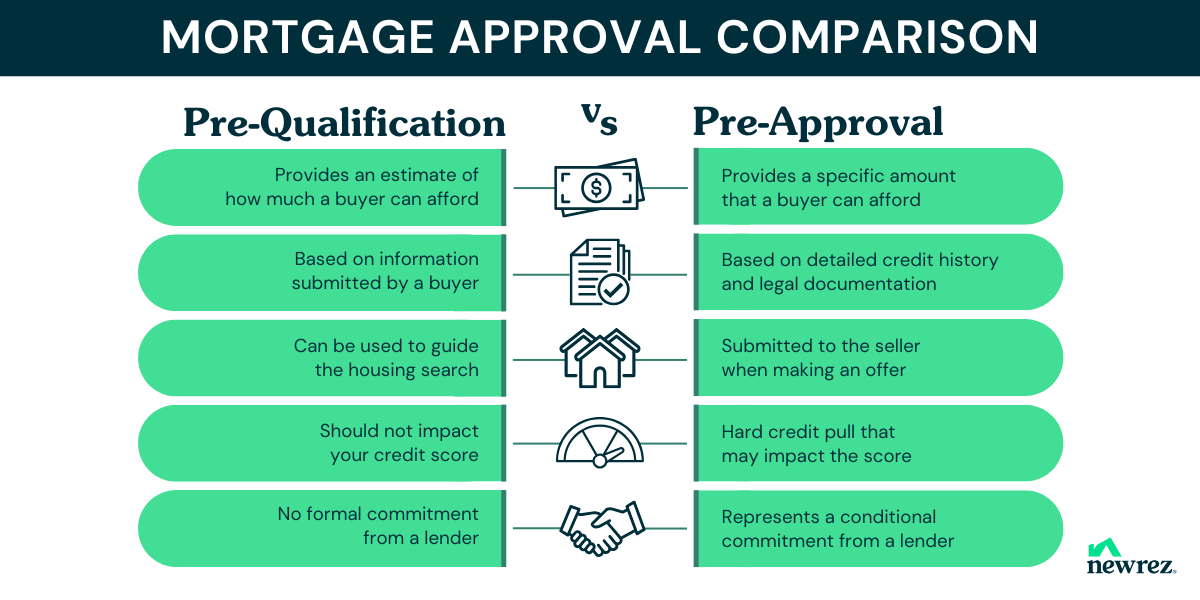

Understanding Loan Pre-Approval vs. Pre-Qualification

Understanding Loan Pre-Approval vs. Pre-Qualification – Buying a home, purchasing a car, or securing a personal loan can be a complex journey. One of the first steps that often confuses people is understanding the difference between loan pre-approval and pre-qualification. While both processes help borrowers gauge how much they might be able to borrow, they serve different purposes and carry different weight with lenders. Knowing the difference can make your borrowing experience smoother and increase your chances of getting the loan you need.

What is Loan Pre-Qualification?

Loan pre-qualification is typically the first step in the borrowing process. It is an informal assessment where a lender reviews basic financial information to estimate how much you might be eligible to borrow. During pre-qualification, you may provide details about your income, debts, assets, and credit history, but this process often does not involve a hard credit check.

Pre-qualification gives borrowers a rough idea of the loan amount they could qualify for. It’s useful for budgeting and planning, especially when shopping for a home or comparing lenders. However, it’s important to understand that pre-qualification does not guarantee loan approval. Lenders can provide an estimate, but until you go through more detailed checks, nothing is final.

Benefits of Pre-Qualification

Pre-qualification is convenient and quick. It helps borrowers understand what loan products may suit their financial situation without committing to a formal application. For first-time homebuyers or anyone exploring financing options, it offers a clear starting point. Since the process is informal, it usually doesn’t affect your credit score, making it a low-risk way to explore your borrowing potential.

What is Loan Pre-Approval?

Loan pre-approval is a more formal and in-depth process. Unlike pre-qualification, pre-approval requires a detailed review of your financial history and often includes a hard credit check. Lenders will verify your income, employment status, debts, and assets, and may request supporting documentation such as tax returns, pay stubs, and bank statements.

Once pre-approved, you receive a conditional commitment from the lender stating the maximum loan amount they are willing to offer. This conditional approval is usually valid for a limited time, giving you a clear understanding of your budget when making major purchases like buying a house. Pre-approval shows sellers and lenders that you are a serious borrower, which can be an advantage in competitive markets.

Advantages of Pre-Approval

Pre-approval provides certainty and confidence. Knowing exactly how much you can borrow allows you to focus your search on options within your budget. It also gives you negotiating power with sellers, as they can see that you have secured financing. For buyers in fast-moving markets, pre-approval can be the difference between winning a bid and missing out on a property.

When to Consider Pre-Qualification

Pre-qualification is ideal for those just beginning their borrowing journey or exploring their options. If you are unsure about your financial readiness or want to compare different lenders, pre-qualification can give you a clear starting point. It’s also helpful for understanding what loan products you might qualify for, which can guide your financial planning.

For example, a first-time homebuyer might seek pre-qualification to determine how much house they can afford. This step allows them to refine their budget and focus on properties within their financial reach without the pressure of a formal application.

When to Consider Pre-Approval

Pre-approval is the logical next step when you are serious about making a purchase. If you are ready to start house hunting, buy a car, or make any significant financial commitment, pre-approval provides a stronger position. Sellers and lenders take pre-approved buyers more seriously, and you gain clarity on your budget and loan terms.

In competitive markets, pre-approval can speed up the purchasing process and prevent delays. Since the lender has already verified your financial situation, closing a deal can be faster once you make an offer. This makes pre-approval especially valuable in real estate or high-demand vehicle purchases.

Tips for a Smooth Pre-Approval Process

-

Check Your Credit Score: Before applying, ensure your credit report is accurate. Correcting errors can improve your chances of approval.

-

Gather Documentation: Prepare pay stubs, tax returns, bank statements, and other financial records in advance.

-

Reduce Debt: Lowering your debt-to-income ratio can increase the loan amount you are eligible for.

-

Avoid New Credit Applications: Taking on new loans or credit cards can affect your pre-approval outcome.

Following these steps can make the pre-approval process faster, smoother, and more likely to result in favorable loan terms.

Conclusion: Choosing the Right Step for Your Situation

Understanding the difference between pre-qualification and pre-approval is crucial for any borrower. Pre-qualification provides a helpful overview of your borrowing potential without commitments, while pre-approval offers a verified and conditional loan amount that strengthens your position in financial negotiations. By knowing when and how to use each option, you can plan your purchases more effectively, make informed financial decisions, and increase your chances of securing the loan you need.

Whether you are entering the housing market for the first time or planning a major purchase, starting with pre-qualification and moving to pre-approval ensures that you approach the process with confidence and clarity. Taking these steps strategically can save time, reduce stress, and ultimately help you achieve your financial goals.

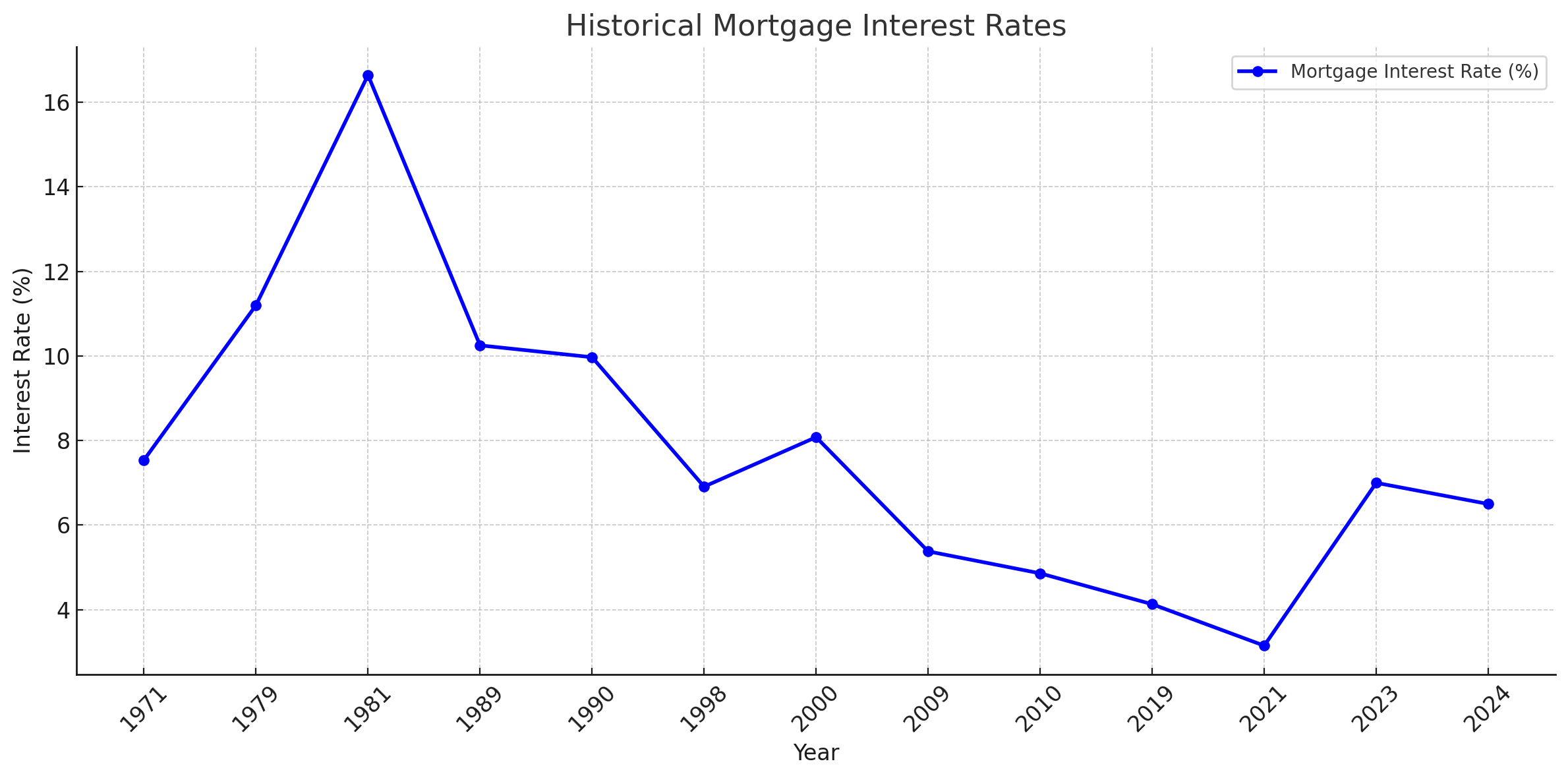

Home Loan Trends from the Past Property Era

2026 Home Loan Tips: Trends, Rates & Application Hacks

2026 Home Loan Tips: Trends, Rates & Application Hacks – The home loan landscape in 2026 looks very different compared to just a few years ago. Buyers are more informed, lenders are more selective, and technology is deeply embedded in almost every step of the mortgage process. Whether you’re a first-time buyer or someone looking to refinance, understanding how home loans work in 2026 can save you thousands of dollars and months of frustration.

This guide breaks down the latest home loan trends, what to expect from interest rates, and practical application hacks that can improve your approval chances.

The Home Loan Market in 2026

The housing market has matured after years of volatility. In 2026, stability is the keyword most lenders and borrowers are using. While prices are no longer skyrocketing overnight, demand for housing remains strong in most regions.

Banks and non-bank lenders have adjusted their strategies. Risk assessments are tighter, but competition between lenders is still alive. This balance creates opportunities for borrowers who come prepared.

Digital-First Mortgage Processes

One of the biggest shifts in 2026 is how digital the home loan journey has become. Paper-based applications are nearly gone. Most lenders now use automated income verification, open banking data, and AI-powered credit assessments.

For borrowers, this means faster approvals, but also less room for inconsistencies. Any mismatch in your financial data can raise red flags instantly. Accuracy matters more than ever.

Home Loan Interest Rates: What to Expect in 2026

Interest rates in 2026 are relatively stable compared to the aggressive hikes seen in earlier years. Central banks have shifted focus from inflation control to economic balance, which has helped calm rate fluctuations.

That said, rates are not identical across lenders, and the gap between advertised rates and approved rates can be significant.

Fixed vs Variable Loans in 2026

Fixed-rate home loans are popular among borrowers who value predictability. In 2026, fixed terms are often shorter, commonly two to three years, giving borrowers flexibility to refinance if market conditions improve.

Variable-rate loans remain attractive for those comfortable with moderate risk. Many lenders now offer hybrid products that allow partial fixing while keeping the rest variable, giving borrowers more control over their repayments.

Credit Score Impact on Your Rate

Your credit score still plays a massive role in determining your interest rate. In 2026, lenders rely heavily on behavioral data, not just traditional credit reports. Payment consistency, account balances, and spending patterns can all influence your final rate.

Improving your credit profile even six months before applying can make a noticeable difference in loan pricing.

Home Loan Application Hacks That Actually Work

Applying for a home loan in 2026 is less about luck and more about preparation. Small adjustments before submitting your application can dramatically improve your approval odds.

Clean Up Your Financial Profile Early

Lenders typically analyze at least six to twelve months of financial history. Reducing unnecessary subscriptions, avoiding impulsive purchases, and keeping stable balances sends a strong signal of reliability.

Job stability also matters. Frequent job changes may not disqualify you, but lenders prefer consistent income streams, especially for higher loan amounts.

Lower Your Debt-to-Income Ratio

One of the most overlooked factors in home loan approval is the debt-to-income ratio. Even if your income is high, excessive existing debt can limit how much you can borrow.

Paying down credit cards, personal loans, or buy-now-pay-later balances before applying can unlock better loan terms and higher borrowing capacity.

Get Pre-Approval the Smart Way

Pre-approval is still a powerful tool in 2026, but it needs to be done carefully. Multiple pre-approval checks across different lenders can hurt your credit score.

Working with a mortgage broker or shortlisting two or three lenders before applying helps reduce unnecessary credit inquiries while still giving you options.

Refinancing Trends in 2026

Refinancing is no longer just about chasing lower rates. In 2026, homeowners refinance to restructure debt, access equity, or switch to more flexible loan products.

Many lenders offer streamlined refinancing processes with minimal documentation for borrowers with strong repayment histories. This makes refinancing faster and cheaper than ever before.

When Refinancing Makes Sense

Refinancing can be a smart move if your financial situation has improved, property value has increased, or your current loan features no longer fit your needs.

However, refinancing solely for a small rate reduction may not always be worth it once fees and reset terms are considered. Running the numbers carefully is essential.

Common Home Loan Mistakes to Avoid

Despite easier access to information, many borrowers still make avoidable mistakes during the home loan process.

Overestimating borrowing capacity is a common issue. Just because a lender approves a certain amount does not mean it fits your lifestyle or long-term goals.

Another frequent mistake is ignoring loan features. Offset accounts, redraw facilities, and repayment flexibility can have a bigger impact over time than a slightly lower interest rate.

How to Position Yourself for Success in 2026

The most successful borrowers in 2026 treat home loans as a long-term financial strategy, not just a transaction. They plan ahead, understand lender expectations, and remain flexible.

Staying informed about market trends, reviewing your loan regularly, and maintaining a healthy financial profile will keep you in a strong position whether you’re buying, refinancing, or investing.

Final Thoughts on Home Loans in 2026

Home loans in 2026 are faster, smarter, and more data-driven than ever before. While the process may seem strict, borrowers who prepare properly can access competitive rates and flexible loan structures.

Understanding current trends, keeping an eye on interest rate movements, and applying smart financial habits will give you a clear advantage. In a market where lenders value transparency and consistency, being prepared is the ultimate application hack.

Home Loans That Haunt: Debt Traps and Long-Term Burdens

Home Loans That Haunt: Debt Traps and Long-Term Burdens – Buying a home is often seen as a milestone of financial success and stability. For many, taking out a home loan is the only way to make this dream a reality. However, not all home loans are created equal. Some loans, despite appearing manageable at first, can quickly turn into debt traps, leaving homeowners with long-term financial burdens that are difficult to escape.

Understanding how these loans work, why they become problematic, and how to avoid them is essential for anyone considering borrowing to buy a home. This guide explores the risks of debt-heavy home loans and offers practical advice for making safer, smarter choices.

How Home Loans Can Become Debt Traps

At first glance, a home loan may seem like a straightforward way to buy property. The monthly payments appear manageable, and lenders often highlight attractive features like low initial interest rates. But hidden costs, complex terms, and poor financial planning can turn a seemingly good deal into a long-term nightmare.

Debt traps often start with loans that offer minimal payments at the beginning but balloon over time. Adjustable rates, deferred interest, or interest-only periods can leave borrowers facing unexpectedly high repayments in the future. Without careful planning, these loans become burdens that stretch over decades, affecting personal finances, savings, and lifestyle.

The Role of High-Interest and Hidden Fees

Many homeowners underestimate how interest and fees accumulate over time. Even a small difference in interest rates can result in thousands of dollars paid over the life of the loan. Some lenders also include hidden charges for administrative costs, early repayments, or late fees, which compound financial stress.

Loans with variable or adjustable rates carry the additional risk of increasing payments. A sudden rise in interest can push monthly installments beyond what the borrower can comfortably manage, leading to late payments, penalties, and long-term debt accumulation.

Common Characteristics of Risky Home Loans

Not every home loan carries the same risk. Certain types of loans are more likely to create financial burdens that last for decades. Recognizing these characteristics can help buyers avoid falling into a debt trap.

Interest-Only and Low-Initial Payment Loans

Interest-only loans allow borrowers to pay just the interest for a set period, usually a few years. While this reduces monthly payments initially, it does not reduce the principal amount borrowed. When the interest-only period ends, payments increase dramatically, catching many borrowers off guard.

Loans with low initial payments may also be marketed as “affordable” options. However, once promotional rates expire, monthly repayments rise significantly, creating financial strain.

Loans With Complex Terms and Fine Print

Some home loans come with clauses that are difficult to understand but have significant long-term consequences. Adjustable-rate loans, balloon payments, and variable fees are common examples. Borrowers who fail to fully grasp these terms may find themselves unprepared for sudden repayment hikes or additional charges.

Lenders often disclose these terms, but in fine print that many people overlook. Carefully reviewing loan agreements and asking questions before signing can prevent unexpected debt traps.

Planning Ahead to Avoid Long-Term Financial Burdens

Avoiding debt traps starts before signing any loan agreement. Planning, research, and realistic assessment of financial capacity are key. Understanding both the short-term and long-term implications of a loan ensures that homeownership remains a positive experience rather than a burden.

Budgeting for True Costs of Homeownership

Monthly repayments are only part of the financial picture. Taxes, insurance, maintenance, and unexpected repairs all add to the cost of owning a home. Borrowers who plan their budgets with these factors in mind are better equipped to manage repayments even if interest rates increase.

A detailed financial plan also helps determine what size of loan is realistically manageable. It may mean borrowing less than the maximum the bank offers, but it prevents financial strain over the long term.

Improving Credit and Financial Health

A strong credit profile not only increases approval chances but also helps secure lower interest rates. High debt-to-income ratios, poor credit history, or unstable income can push borrowers toward higher-risk loans with unfavorable terms.

Taking time to pay down existing debts, improving credit scores, and maintaining consistent income can make a significant difference in securing safer, more affordable home loans.

Red Flags to Watch Out For

Certain warning signs indicate that a home loan may become a long-term burden. Recognizing these early can save borrowers from years of financial stress.

High-interest rates that are significantly above market averages, loans requiring frequent adjustments, or offers with complex repayment schedules are common red flags. Additionally, loans that promise unusually low initial payments often come with hidden costs or future spikes in repayment.

Consulting with a financial advisor or mortgage expert can provide clarity. They can help evaluate whether a loan is sustainable or if it carries risks that outweigh short-term benefits.

Strategies to Escape or Avoid Debt Traps

For those already facing challenging home loan terms, there are strategies to mitigate long-term burdens. Refinancing, consolidating debts, or switching to fixed-rate loans can reduce monthly payments and provide stability. Early repayment of high-interest loans, if financially feasible, also lowers long-term costs.

Education and awareness are the best preventative strategies. Borrowers who take time to understand loan terms, anticipate future financial changes, and plan accordingly are far less likely to fall into debt traps.

Choosing Loans That Align With Long-Term Goals

A home loan should support long-term financial stability rather than create ongoing stress. Choosing loans with predictable payments, transparent fees, and terms that match income and lifestyle ensures a manageable repayment journey.

Flexible repayment options, the ability to make extra payments without penalties, and loans that avoid sudden spikes in costs help homeowners maintain financial control. Thinking beyond short-term affordability prevents the haunting burden of long-term debt.

Final Thoughts on Home Loans and Financial Responsibility

Homeownership should be a step toward financial growth and security, not a lifelong debt trap. Understanding the risks, planning carefully, and choosing loans wisely are essential to prevent long-term burdens.

Loans that appear affordable at first may hide future challenges. By budgeting realistically, improving financial health, and analyzing loan terms thoroughly, borrowers can make choices that protect their future and allow homeownership to remain a rewarding experience.

Being proactive and informed transforms borrowing from a potential liability into a strategic investment. Awareness, planning, and caution are the keys to escaping debt traps and building a home that is truly a place of comfort, not financial worry.