Understanding Loan Pre-Approval vs. Pre-Qualification

Understanding Loan Pre-Approval vs. Pre-Qualification – Buying a home, purchasing a car, or securing a personal loan can be a complex journey. One of the first steps that often confuses people is understanding the difference between loan pre-approval and pre-qualification. While both processes help borrowers gauge how much they might be able to borrow, they serve different purposes and carry different weight with lenders. Knowing the difference can make your borrowing experience smoother and increase your chances of getting the loan you need.

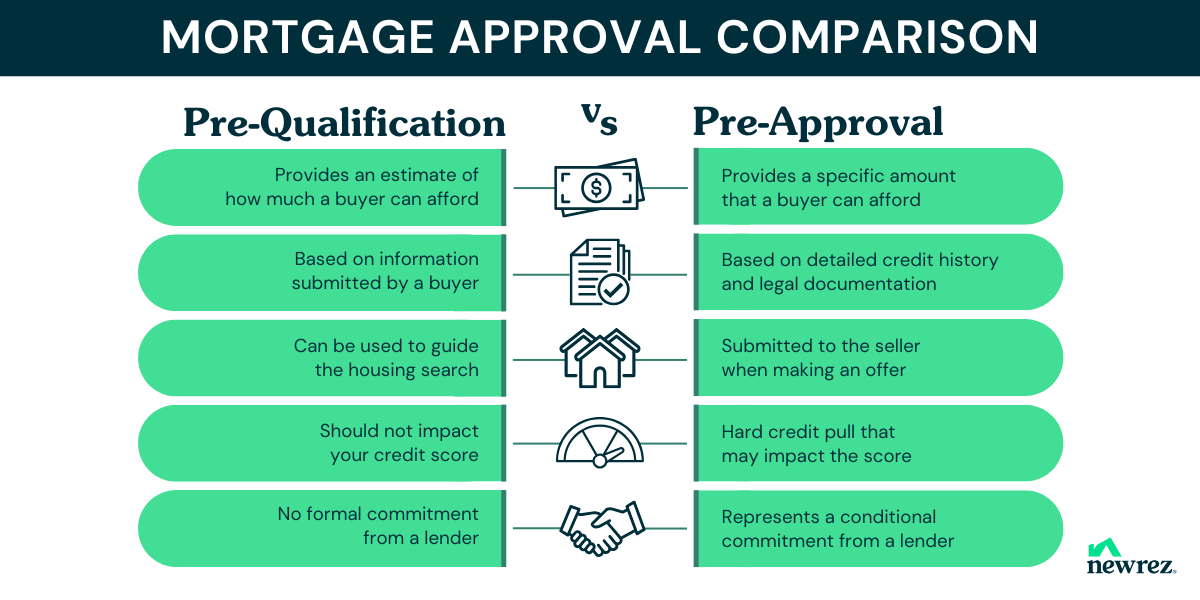

What is Loan Pre-Qualification?

Loan pre-qualification is typically the first step in the borrowing process. It is an informal assessment where a lender reviews basic financial information to estimate how much you might be eligible to borrow. During pre-qualification, you may provide details about your income, debts, assets, and credit history, but this process often does not involve a hard credit check.

Pre-qualification gives borrowers a rough idea of the loan amount they could qualify for. It’s useful for budgeting and planning, especially when shopping for a home or comparing lenders. However, it’s important to understand that pre-qualification does not guarantee loan approval. Lenders can provide an estimate, but until you go through more detailed checks, nothing is final.

Benefits of Pre-Qualification

Pre-qualification is convenient and quick. It helps borrowers understand what loan products may suit their financial situation without committing to a formal application. For first-time homebuyers or anyone exploring financing options, it offers a clear starting point. Since the process is informal, it usually doesn’t affect your credit score, making it a low-risk way to explore your borrowing potential.

What is Loan Pre-Approval?

Loan pre-approval is a more formal and in-depth process. Unlike pre-qualification, pre-approval requires a detailed review of your financial history and often includes a hard credit check. Lenders will verify your income, employment status, debts, and assets, and may request supporting documentation such as tax returns, pay stubs, and bank statements.

Once pre-approved, you receive a conditional commitment from the lender stating the maximum loan amount they are willing to offer. This conditional approval is usually valid for a limited time, giving you a clear understanding of your budget when making major purchases like buying a house. Pre-approval shows sellers and lenders that you are a serious borrower, which can be an advantage in competitive markets.

Advantages of Pre-Approval

Pre-approval provides certainty and confidence. Knowing exactly how much you can borrow allows you to focus your search on options within your budget. It also gives you negotiating power with sellers, as they can see that you have secured financing. For buyers in fast-moving markets, pre-approval can be the difference between winning a bid and missing out on a property.

When to Consider Pre-Qualification

Pre-qualification is ideal for those just beginning their borrowing journey or exploring their options. If you are unsure about your financial readiness or want to compare different lenders, pre-qualification can give you a clear starting point. It’s also helpful for understanding what loan products you might qualify for, which can guide your financial planning.

For example, a first-time homebuyer might seek pre-qualification to determine how much house they can afford. This step allows them to refine their budget and focus on properties within their financial reach without the pressure of a formal application.

When to Consider Pre-Approval

Pre-approval is the logical next step when you are serious about making a purchase. If you are ready to start house hunting, buy a car, or make any significant financial commitment, pre-approval provides a stronger position. Sellers and lenders take pre-approved buyers more seriously, and you gain clarity on your budget and loan terms.

In competitive markets, pre-approval can speed up the purchasing process and prevent delays. Since the lender has already verified your financial situation, closing a deal can be faster once you make an offer. This makes pre-approval especially valuable in real estate or high-demand vehicle purchases.

Tips for a Smooth Pre-Approval Process

-

Check Your Credit Score: Before applying, ensure your credit report is accurate. Correcting errors can improve your chances of approval.

-

Gather Documentation: Prepare pay stubs, tax returns, bank statements, and other financial records in advance.

-

Reduce Debt: Lowering your debt-to-income ratio can increase the loan amount you are eligible for.

-

Avoid New Credit Applications: Taking on new loans or credit cards can affect your pre-approval outcome.

Following these steps can make the pre-approval process faster, smoother, and more likely to result in favorable loan terms.

Conclusion: Choosing the Right Step for Your Situation

Understanding the difference between pre-qualification and pre-approval is crucial for any borrower. Pre-qualification provides a helpful overview of your borrowing potential without commitments, while pre-approval offers a verified and conditional loan amount that strengthens your position in financial negotiations. By knowing when and how to use each option, you can plan your purchases more effectively, make informed financial decisions, and increase your chances of securing the loan you need.

Whether you are entering the housing market for the first time or planning a major purchase, starting with pre-qualification and moving to pre-approval ensures that you approach the process with confidence and clarity. Taking these steps strategically can save time, reduce stress, and ultimately help you achieve your financial goals.