Home Loan Trends from the Past Property Era

Home Loan Trends from the Past Property Era – The property market has always moved in cycles. From booming real estate eras to sudden downturns, each phase has shaped how home loans are designed, marketed, and approved. Looking back at past property eras gives us valuable insight into why mortgage trends today look the way they do—and what buyers, investors, and lenders can learn moving forward.

In this article, we’ll explore the evolution of home loan trends across historical property cycles and how those shifts continue to influence modern mortgage strategies.

The Early Property Boom and Traditional Home Loans

In earlier property eras, home loans were relatively simple. Banks relied heavily on manual underwriting, strict income verification, and conservative lending criteria. Borrowers often needed substantial down payments, stable employment, and a strong financial history.

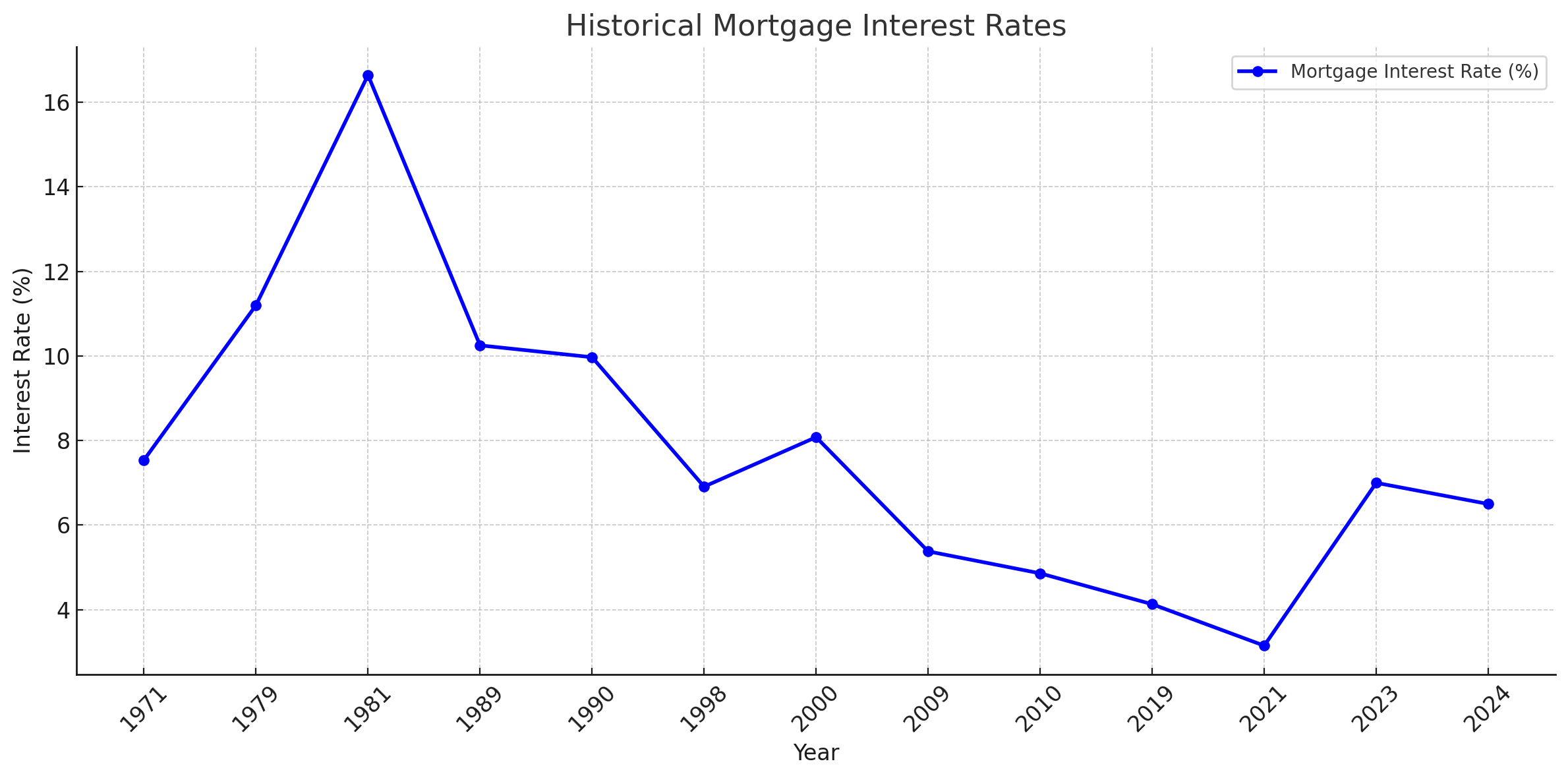

Interest rates during these periods were generally higher, but the lending process was more cautious. Banks viewed mortgages as long-term commitments and prioritized minimizing risk over expanding their customer base. As a result, home ownership grew steadily but slowly, driven by genuine affordability rather than speculative demand.

This conservative approach helped stabilize property markets, but it also limited access for many first-time buyers.

The Rise of Aggressive Lending in the Expansion Era

As global economies grew and property markets expanded, home loan trends shifted dramatically. Financial institutions began introducing innovative mortgage products to attract more borrowers. Adjustable-rate mortgages, low down payment options, and interest-only loans became popular tools to boost home ownership.

During this era, lenders focused on volume. Property prices were rising rapidly, and the belief that real estate values would always increase encouraged both buyers and lenders to take more risks. Home loans became easier to obtain, credit standards loosened, and marketing campaigns emphasized fast approvals and minimal documentation.

This period marked a turning point where mortgages became not just financial products but also growth engines for the broader economy.

The Impact of the Property Bubble and Financial Crisis

The aggressive lending practices of the expansion era eventually contributed to major property bubbles in several regions. When housing prices peaked and began to fall, many borrowers found themselves with mortgages that exceeded the value of their homes.

The financial crisis that followed reshaped the global mortgage industry. Banks suffered massive losses, governments intervened, and regulators introduced stricter lending rules. Home loan trends shifted back toward conservative underwriting, with greater emphasis on borrower verification, debt-to-income ratios, and risk assessment.

This era taught lenders and policymakers that unchecked mortgage growth could destabilize entire economies.

Post-Crisis Mortgage Reforms and Modern Lending Standards

After the crisis, the home loan market entered a reform phase. Governments introduced tighter regulations, consumer protection laws, and transparency requirements. Lenders adopted more sophisticated risk models and automated underwriting systems to balance accessibility with stability.

Interest rates dropped significantly in many countries as central banks implemented monetary stimulus measures. This created a new wave of home buyers who benefited from historically low mortgage rates. Fixed-rate loans became more popular, and refinancing surged as borrowers sought to lock in favorable terms.

Technology also transformed mortgage applications. Digital platforms simplified documentation, accelerated approvals, and improved customer experience, making home loans more accessible without repeating the excesses of the past.

The Influence of Demographic Shifts on Home Loan Trends

Changing demographics have also played a major role in shaping mortgage markets. Millennials and Gen Z buyers entered the property market with different expectations than previous generations. They value flexibility, digital services, and transparent pricing.

As a result, lenders introduced flexible repayment plans, hybrid mortgage products, and online mortgage platforms. Urbanization trends, remote work, and lifestyle preferences have also influenced where people buy homes and how they finance them.

These demographic factors continue to drive innovation in the mortgage industry.

The Role of Investors in Past Property Eras

Property investors have always influenced home loan trends. During boom periods, investors often leveraged multiple mortgages to expand their portfolios. This increased demand for buy-to-let loans and specialized mortgage products designed for rental properties.

In some past eras, speculative investment amplified price growth, contributing to market volatility. Today, lenders often apply stricter criteria for investment properties to reduce systemic risk, reflecting lessons learned from previous cycles.

Lessons from Historical Mortgage Cycles

Looking back at past property eras reveals recurring patterns in home loan trends. When lending is too strict, home ownership growth slows. When lending becomes too loose, property bubbles form. The challenge for modern lenders is finding the right balance between accessibility and stability.

One key lesson is the importance of transparency. Borrowers today are more informed, and regulators demand clear disclosure of terms, fees, and risks. Another lesson is the value of long-term affordability, not just initial monthly payments.

Sustainable home ownership depends on realistic financial planning and responsible lending practices.

How Past Trends Shape Today’s Mortgage Strategies

Modern home loan products reflect decades of evolution. Fixed and adjustable-rate mortgages coexist, offering borrowers choices based on risk tolerance and market conditions. Digital underwriting tools analyze data in real time, reducing approval times while maintaining compliance.

Lenders now use historical data to stress-test mortgage portfolios against potential economic downturns. This proactive approach aims to prevent future crises and ensure the resilience of the housing market.

Additionally, environmental and social factors are influencing mortgage trends. Green mortgages, energy-efficient home incentives, and inclusive lending programs are emerging as part of a broader shift toward sustainable property finance.

The Future Outlook for Home Loans

As property markets continue to evolve, home loan trends will adapt to economic conditions, technology, and consumer behavior. Artificial intelligence, blockchain, and open banking may further transform mortgage processing and risk assessment.

However, the fundamental lessons from past property eras remain relevant. Responsible lending, informed borrowing, and regulatory oversight are essential to maintaining stable housing markets.

Understanding historical mortgage cycles helps buyers and investors make smarter decisions. It also helps lenders design products that support long-term home ownership rather than short-term market expansion.

Final Thoughts on Home Loan Trends from the Past Property Era

The history of home loans is closely tied to the evolution of property markets. From conservative lending in early eras to aggressive expansion and post-crisis reforms, each phase has left a lasting impact on how mortgages function today.

By examining these trends, we gain insight into the balance between innovation and risk, growth and stability. For anyone involved in real estate—whether buyers, investors, or financial institutions—understanding these historical patterns is a powerful tool for navigating the future of property finance.

Home loans are more than just financial contracts; they reflect economic cycles, social change, and technological progress. And as the property market enters new eras, the lessons from the past will continue to shape the mortgages of tomorrow.