How to Negotiate Your Home Loan Terms With Lenders – Buying a home is one of the biggest financial decisions most people will make in their lifetime. While finding the perfect property is exciting, negotiating the terms of your home loan is equally important. Many borrowers accept the first loan offer they receive, but understanding how to negotiate with lenders can save you thousands of dollars over the life of the mortgage. With the right approach, preparation, and knowledge, you can secure favorable interest rates, lower fees, and flexible repayment options that suit your financial goals.

Why Negotiating Your Home Loan Matters

A home loan is a long-term commitment, often lasting 15 to 30 years. Even a small reduction in interest rates or fees can make a significant difference in your monthly payments and total interest paid. Negotiating your loan terms allows you to gain control over costs, reduce financial stress, and customize your mortgage to fit your needs. Lenders often have some flexibility, especially for borrowers with strong credit scores, stable income, and a clear understanding of the market. Knowing your leverage and approaching the conversation strategically can put you in a strong position.

Understand Your Financial Position

Before entering negotiations, it’s essential to have a clear picture of your financial situation. Lenders will consider your credit score, income, debt-to-income ratio, and employment stability when determining the terms of your loan. By reviewing your finances in advance, you can identify areas that may improve your negotiation power. For instance, paying down high-interest debts or correcting errors on your credit report can boost your creditworthiness. Understanding your finances also helps you determine the type of mortgage you can realistically afford and the monthly payments that fit your budget.

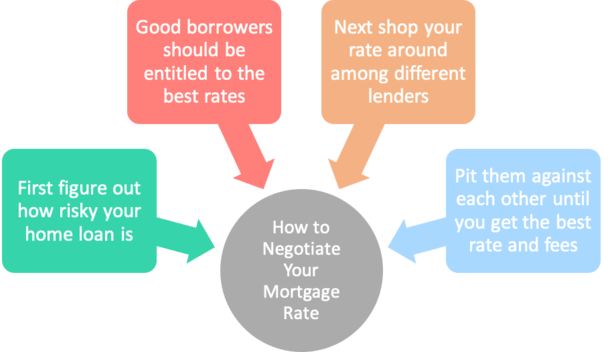

Check Your Credit Score

Your credit score is one of the most critical factors in home loan negotiations. Lenders use it to assess risk and decide on interest rates. A higher credit score often translates into lower rates and more favorable terms. Before negotiating, check your credit report for inaccuracies, pay down outstanding balances, and avoid taking on new loans. Demonstrating financial responsibility can increase a lender’s willingness to offer better terms.

Compare Loan Offers

Not all lenders offer the same rates or conditions, so shopping around is a key step in negotiation. Comparing multiple loan offers gives you leverage when discussing terms with your preferred lender. By showing that you have options, you signal that you are an informed borrower and can walk away if terms are not favorable. Pay attention to interest rates, origination fees, closing costs, and repayment flexibility when evaluating offers. Even small differences in rates can save you significant amounts over the life of your mortgage.

Consider Different Loan Types

Lenders provide a variety of loan options, including fixed-rate, adjustable-rate, and interest-only mortgages. Each type comes with different benefits and risks. Understanding the options allows you to negotiate terms that align with your long-term financial goals. For example, a fixed-rate mortgage offers predictable monthly payments, while an adjustable-rate mortgage may provide lower initial rates but can fluctuate over time. Being informed about these differences strengthens your position in discussions with lenders.

Be Prepared to Ask

Negotiation is not just about waiting for the lender to offer better terms—it involves proactive questions. Ask about interest rate reductions, lower origination fees, or the possibility of waiving certain closing costs. Some lenders may also offer flexible repayment schedules or discounts for automatic payments. By initiating the conversation, you demonstrate that you are an engaged borrower who understands the value of the loan. Lenders may be more willing to accommodate requests when they see that you are serious, organized, and financially responsible.

Leverage Your Strengths

Your financial profile can serve as a powerful tool in negotiation. Stable income, a high credit score, a sizable down payment, or a long-standing relationship with a bank can all be used to your advantage. Highlight these strengths during discussions with your lender. For example, offering a larger down payment might encourage the lender to lower your interest rate, as it reduces their risk. Demonstrating reliability and preparedness can make lenders more flexible in offering favorable terms.

Understand Lender Incentives

Lenders often have incentives to attract borrowers, such as reduced fees for refinancing, special rates for certain customer groups, or promotions for first-time homebuyers. By researching these incentives, you can identify opportunities to negotiate. Understanding what motivates a lender helps you frame your requests in a way that aligns with their goals. This approach can increase the likelihood of achieving better terms without pushing too hard or risking the relationship.

Don’t Rush the Process

Negotiating a home loan is not something to be rushed. Take the time to review offers, ask questions, and understand the implications of different terms. Rushing may lead to missing hidden fees, unfavorable conditions, or long-term costs. Patience allows you to weigh your options carefully and enter discussions with confidence. A well-considered approach shows lenders that you are informed and serious, which can make them more willing to negotiate.

Seek Professional Advice

If you’re unsure about the negotiation process, consider consulting a mortgage broker or financial advisor. Professionals can provide insights into market trends, lender practices, and optimal strategies for negotiation. Their expertise can help you navigate complex loan documents and identify opportunities that might not be immediately apparent. While professional advice may come at a cost, the potential savings from securing better loan terms often outweigh the expense.

Final Thoughts: Negotiation is Key to Savings

Negotiating your home loan terms is an essential step in responsible homeownership. By understanding your financial position, comparing offers, asking informed questions, and leveraging your strengths, you can secure a mortgage that works for you. Lenders have flexibility, and informed borrowers who take the time to negotiate often enjoy lower rates, reduced fees, and more favorable conditions.

Remember, a home loan is a long-term commitment, and every dollar saved in interest or fees matters. Approaching negotiations strategically not only reduces financial strain but also empowers you to make decisions that align with your long-term goals. With preparation, knowledge, and confidence, you can turn the home loan process into an opportunity to gain financial advantage rather than simply a necessary step in buying a property.