Should You Consider a 15-Year vs. 30-Year Home Loan? The Pros and Cons – Choosing between a 15-year vs. 30-year home loan is one of the biggest financial decisions you’ll make when buying a house. For many buyers, the question isn’t just about getting approved for a mortgage. It’s about finding the right balance between monthly affordability and long-term financial freedom.

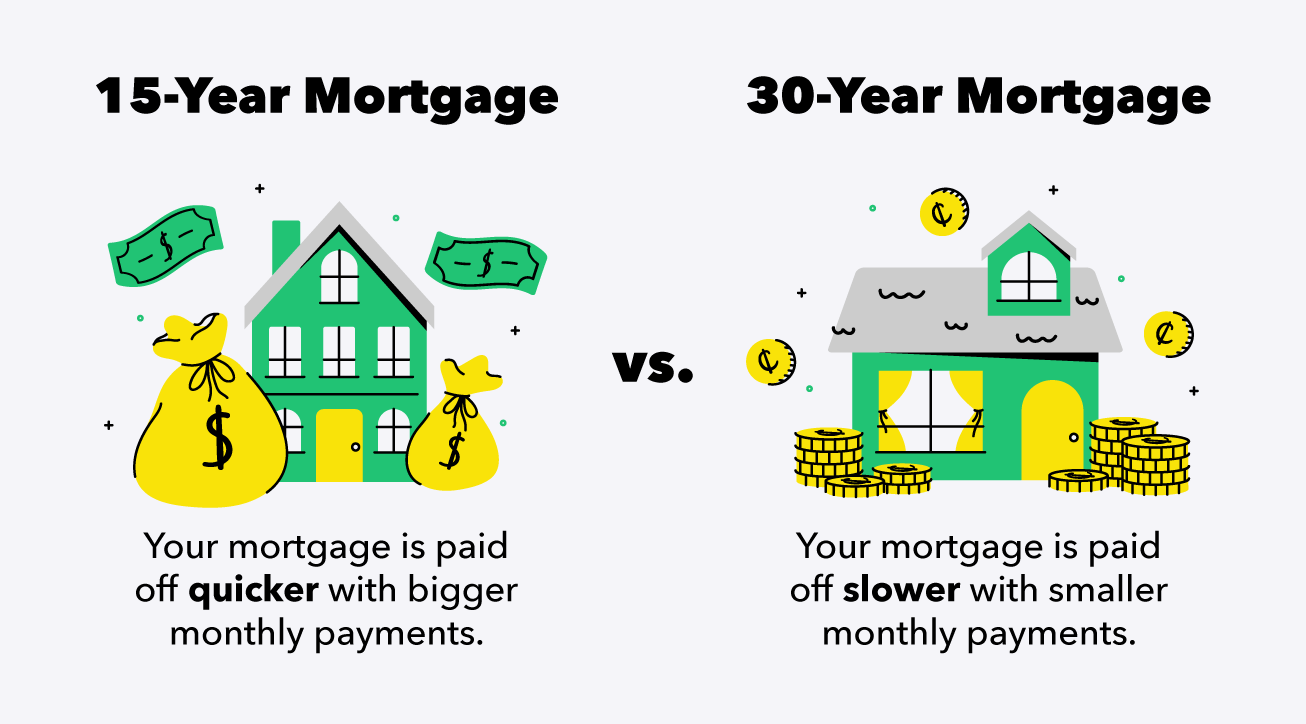

If you’re currently comparing mortgage terms, you’ve probably noticed how different the numbers can look. A 15-year mortgage typically comes with higher monthly payments but lower total interest. A 30-year mortgage, on the other hand, offers lower monthly payments but stretches the loan over a much longer period.

So which one makes more sense for you? Let’s break down the pros and cons of a 15-year vs. 30-year home loan in a way that actually helps you decide.

Understanding the Basics of 15-Year and 30-Year Mortgages

Before diving into the pros and cons, it’s important to understand how these two loan terms work.

A 15-year home loan means you agree to pay off your mortgage in 15 years. Because the repayment period is shorter, lenders usually offer lower interest rates compared to 30-year loans. However, since you’re paying the loan off faster, your monthly mortgage payment will be significantly higher.

A 30-year home loan spreads your payments over 30 years. This longer term reduces your monthly payment, making homeownership more accessible for many buyers. However, you’ll likely pay more in interest over the life of the loan.

When comparing a 15-year vs. 30-year mortgage, the real difference isn’t just the loan term. It’s how each option impacts your cash flow, long-term wealth, and financial flexibility.

The Pros of a 15-Year Home Loan

Lower Interest Rates

One of the biggest advantages of a 15-year mortgage is the lower interest rate. Lenders typically offer better rates because the loan is paid off faster, which reduces their risk.

Even a small difference in interest rates can save you tens of thousands of dollars over time. If your goal is to minimize total interest paid, a 15-year home loan can be a powerful tool.

Less Interest Paid Over Time

Because you’re paying off the principal faster and usually at a lower interest rate, you’ll pay significantly less interest overall. In many cases, homeowners can save a substantial amount compared to a 30-year mortgage.

If building equity quickly is important to you, a 15-year loan allows you to own your home outright much sooner. That means more financial freedom and fewer long-term obligations.

Faster Equity Growth

With a 15-year mortgage, a larger portion of your monthly payment goes toward the principal. This accelerates equity growth, which can be beneficial if you plan to sell the property in the future or use your home equity for other investments.

Owning your home free and clear in 15 years also means you can redirect that monthly payment toward retirement savings, investments, or other financial goals.

The Cons of a 15-Year Home Loan

Higher Monthly Payments

The biggest drawback of a 15-year vs. 30-year home loan comparison is the higher monthly payment required for the shorter term.

For many buyers, this higher payment can strain monthly budgets. It may limit your ability to invest elsewhere, build emergency savings, or handle unexpected expenses comfortably.

Reduced Financial Flexibility

Committing to a higher monthly mortgage payment means less flexibility. If your income changes or you face financial challenges, the higher required payment could feel stressful.

While you may save money in the long run, the short-term pressure isn’t ideal for everyone.

The Pros of a 30-Year Home Loan

Lower Monthly Payments

One of the most attractive features of a 30-year mortgage is affordability. The lower monthly payment allows many buyers to qualify for a larger home or purchase sooner.

For families balancing other financial priorities such as childcare, student loans, or retirement savings, the extra breathing room in monthly cash flow can be extremely valuable.

Greater Cash Flow Flexibility

With lower required payments, you have more control over your money. You can choose to invest the difference, build savings, or even make extra payments when it makes sense.

Some homeowners prefer a 30-year home loan because it gives them options. You’re not locked into a high monthly obligation, but you can still pay extra toward the principal if you want to reduce interest costs.

Easier Qualification

Because the monthly payment is lower, qualifying for a 30-year mortgage is often easier. Lenders look at your debt-to-income ratio, and a smaller payment can improve your approval odds.

For first-time homebuyers especially, the 30-year term can make homeownership more accessible.

The Cons of a 30-Year Home Loan

Higher Total Interest Paid

The biggest downside of a 30-year mortgage is the total interest paid over time. Even if the interest rate difference seems small, stretching payments across 30 years significantly increases the overall cost of the loan.

Over decades, this can add up to a substantial amount of money that could have been used elsewhere.

Slower Equity Building

With a 30-year home loan, a larger portion of your early payments goes toward interest rather than principal. This means it takes longer to build meaningful equity in your property.

If your goal is to own your home quickly or leverage equity for other investments, the longer timeline may not align with your plans.

15-Year vs. 30-Year Home Loan: Which One Is Right for You?

When deciding between a 15-year vs. 30-year mortgage, there isn’t a universal right answer. It depends on your financial situation, goals, and risk tolerance.

If you have stable income, low debt, and a strong emergency fund, a 15-year home loan can help you build wealth faster and reduce long-term interest costs. It’s ideal for buyers who prioritize becoming debt-free quickly.

On the other hand, if you value flexibility, anticipate changes in income, or want to invest in other opportunities, a 30-year mortgage may offer more breathing room. The lower monthly payment can reduce stress and give you greater control over your finances.

Some homeowners choose a middle-ground strategy: taking out a 30-year home loan but making extra principal payments when possible. This approach offers flexibility while still reducing interest over time.

Key Factors to Consider Before Choosing

When comparing a 15-year vs. 30-year home loan, think beyond just the interest rate. Consider your long-term career stability, family plans, investment goals, and lifestyle priorities.

Ask yourself whether you’re comfortable committing to higher monthly payments for 15 years. Consider how the mortgage payment fits into your broader financial strategy, including retirement savings and emergency funds.

Also, evaluate how long you plan to stay in the home. If you expect to move within a few years, the long-term interest savings of a 15-year mortgage may not fully benefit you.

Final Thoughts on 15-Year vs. 30-Year Mortgages

The debate between a 15-year vs. 30-year home loan ultimately comes down to balance. A 15-year mortgage offers faster payoff, lower total interest, and quicker equity growth. A 30-year mortgage provides lower monthly payments, flexibility, and easier qualification.

Neither option is inherently better. The right choice is the one that aligns with your financial comfort level and long-term goals.

Before making a final decision, run the numbers carefully and consider how each loan term fits into your overall financial plan. A home loan is a long-term commitment, but with the right strategy, it can also be a powerful step toward building lasting wealth.