How Rising Property Prices Affect Monthly Mortgage Payments

How Rising Property Prices Affect Monthly Mortgage Payments – The housing market rarely stays still. In many cities around the world, property prices continue to climb year after year. While this trend can benefit homeowners who already own property, it creates a different reality for buyers entering the market. One of the biggest impacts of rising home prices is the direct effect they have on monthly mortgage payments.

For anyone planning to buy a home, understanding how property price growth influences mortgage costs is essential. The relationship between house prices, loan amounts, interest rates, and repayment terms determines how much a homeowner ultimately pays every month. As property values rise, these factors shift in ways that can significantly affect affordability.

This article explores how increasing real estate prices influence monthly mortgage payments, why borrowers often feel the pressure when housing markets surge, and what buyers can do to navigate a more expensive property landscape.

The Connection Between Property Prices and Mortgage Size

When property prices rise, the most immediate effect is the increase in the total loan amount required to purchase a home. Most buyers rely on mortgage financing to afford real estate, which means the higher the home price, the larger the mortgage they need.

For example, if a house that once cost $250,000 rises to $350,000, the required loan increases dramatically, even if the down payment percentage remains the same. A larger loan naturally leads to higher monthly payments because the borrower must repay more principal over time.

Mortgage payments are typically made up of several components. These include the loan principal, interest, property taxes, and sometimes insurance. When the property price increases, the principal portion of the loan rises. This means the monthly repayment amount also climbs, even if the interest rate remains unchanged.

In fast-growing housing markets, this effect becomes more noticeable. Buyers often discover that the same type of home they could afford just a few years ago now requires a significantly higher monthly payment.

How Loan Terms Influence Monthly Payments

The structure of a mortgage loan also plays a major role in determining monthly payments. Most homeowners choose repayment terms that range from 15 to 30 years. The length of the loan spreads the repayment of the borrowed money across many months.

When property prices increase, borrowers sometimes extend their loan terms to reduce the monthly financial burden. A longer mortgage term lowers the payment per month but increases the total interest paid over the life of the loan.

For instance, a buyer facing higher property prices might choose a 30-year mortgage instead of a 20-year option. While this reduces the immediate monthly obligation, it means paying interest for a longer period.

Rising housing prices therefore influence not only the size of the loan but also the way borrowers structure their mortgage strategy.

Interest Rates and Housing Affordability

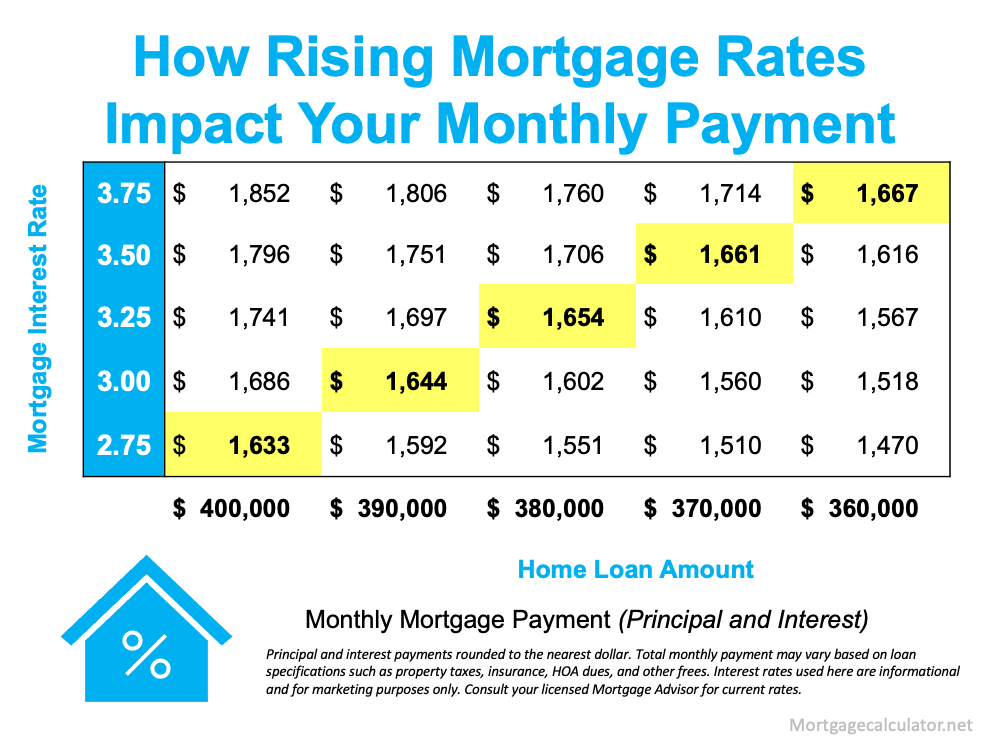

Interest rates are another important factor in the mortgage equation. Even if property prices increase, lower interest rates can sometimes soften the impact on monthly payments. On the other hand, when both property prices and interest rates rise at the same time, affordability becomes a bigger challenge.

Mortgage lenders calculate interest as a percentage of the remaining loan balance. With higher property prices, the loan amount grows, and interest charges are calculated on a larger principal. This results in a noticeable increase in monthly repayments.

For example, a borrower taking a $400,000 mortgage will pay considerably more interest each month than someone borrowing $250,000, even if the interest rate is identical.

Because of this dynamic, rising property values often push buyers to closely monitor interest rate trends before committing to a mortgage.

The Role of Down Payments

Another key factor affected by rising property prices is the size of the down payment. Most lenders require buyers to contribute a portion of the home’s price upfront. This is usually expressed as a percentage of the purchase price, often around 10% to 20%.

As home prices climb, the amount required for a down payment also increases. Buyers must save more money before entering the housing market, and those who cannot afford a larger upfront payment may end up borrowing more.

A smaller down payment leads to a larger mortgage balance. In turn, this increases the monthly mortgage payment because the borrower is financing a greater portion of the property value.

In competitive housing markets, some buyers reduce their down payment simply to enter the market sooner. While this strategy may secure a home purchase, it often results in higher monthly mortgage obligations.

Property Taxes and Insurance Costs

Rising property prices affect more than just the mortgage principal. They also influence related costs such as property taxes and homeowners insurance. These expenses are often included in the total monthly mortgage payment.

Local governments typically assess property taxes based on the value of a home. When property values increase, tax assessments may rise as well. This means homeowners pay more each year, and the additional cost is often reflected in their monthly mortgage escrow payments.

Similarly, insurance premiums can increase when property values climb because the cost to rebuild or repair the home becomes higher. Lenders often require borrowers to maintain adequate insurance coverage, which adds another layer to the monthly housing expense.

Together, these factors mean that rising property prices can gradually increase the overall cost of homeownership, even after the initial purchase.

Market Competition and Buyer Pressure

Another reason rising property prices affect mortgage payments is market competition. In high-demand areas, buyers frequently bid above the asking price to secure a property. This practice drives home values even higher and pushes mortgage amounts upward.

When multiple buyers compete for limited housing inventory, sellers gain more negotiating power. As a result, properties may sell for prices well above historical averages.

For buyers relying on mortgage financing, this means accepting a larger loan than originally planned. Higher purchase prices translate into larger monthly payments, which can stretch household budgets.

This competitive environment is common in growing cities and popular residential areas where demand continues to outpace supply.

Strategies Buyers Use to Manage Higher Mortgage Payments

Despite rising property prices, many buyers still find ways to enter the housing market. One common strategy involves adjusting expectations about property size or location. Choosing a smaller home or a property in a more affordable neighborhood can help reduce the required mortgage amount.

Another approach is improving credit scores before applying for a mortgage. Borrowers with strong credit profiles often qualify for lower interest rates, which can reduce monthly payments even if property prices are high.

Some buyers also increase their down payment to offset rising home values. By contributing more money upfront, they reduce the total loan balance and lower their monthly mortgage obligations.

In addition, exploring different mortgage products can help buyers find repayment structures that match their financial situation.

Long-Term Effects of Rising Property Values

While rising property prices increase mortgage payments in the short term, they can also create long-term financial benefits for homeowners. As property values appreciate, homeowners build equity in their homes.

Equity represents the difference between the property’s market value and the remaining mortgage balance. Over time, as borrowers continue making payments and property values increase, this equity grows.

Homeowners can sometimes access this equity through refinancing or home equity loans, providing financial flexibility for future investments or expenses.

However, the key challenge remains the initial affordability. Rising property prices make it harder for new buyers to enter the market and often require higher monthly mortgage commitments.

Understanding the Bigger Picture

The relationship between property prices and mortgage payments highlights how closely housing affordability is tied to market conditions. When home values rise, buyers typically need larger loans, higher down payments, and stronger financial preparation.

Monthly mortgage payments increase because the borrowed amount grows, interest charges expand, and related costs such as taxes and insurance follow the upward trend of property values.

For prospective homeowners, understanding these dynamics can help them plan more effectively. Monitoring housing trends, improving financial readiness, and exploring flexible mortgage options can make the path to homeownership more manageable, even in markets where property prices continue to climb.

In the end, rising property prices reshape the housing landscape. While they may increase monthly mortgage payments, they also reflect the ongoing demand for real estate and the long-term value many people place on owning a home.

How to Choose Between Conventional and Government

How to Choose Between Conventional and Government-Backed Home Loans – Buying a home is one of the biggest financial decisions you’ll ever make. For most people, that means choosing the right mortgage. If you’ve started researching, you’ve probably come across two main options: conventional home loans and government-backed home loans. At first glance, they may seem similar. Both help you finance a house. Both require approval from a lender. But the differences can significantly affect your monthly payments, upfront costs, and long-term financial health.

Understanding how to choose between conventional and government-backed home loans is crucial before signing any paperwork. The right choice depends on your credit score, income stability, savings, and long-term plans.

What Is a Conventional Home Loan?

A conventional home loan is a mortgage that is not insured or guaranteed by the federal government. Instead, it follows guidelines set by government-sponsored enterprises like Fannie Mae and Freddie Mac. These organizations buy loans from lenders, which helps keep the mortgage market stable and accessible.

Because conventional loans are not backed by the government, lenders take on more risk. That usually means stricter requirements for borrowers. You typically need a higher credit score, stable income, and a lower debt-to-income ratio to qualify.

However, if you meet those standards, a conventional mortgage can be a very cost-effective option. You may benefit from lower overall borrowing costs and fewer long-term fees compared to some government-backed programs.

What Is a Government-Backed Home Loan?

Government-backed home loans are insured or guaranteed by federal agencies. This reduces the risk for lenders and makes it easier for borrowers to qualify.

Some of the most common types include:

Loans insured by the Federal Housing Administration, often called FHA loans. These are popular among first-time homebuyers and borrowers with lower credit scores.

Loans guaranteed by the Department of Veterans Affairs, known as VA loans. These are available to eligible veterans, active-duty service members, and certain military spouses.

Loans backed by the United States Department of Agriculture, often referred to as USDA loans. These are designed for buyers in eligible rural and suburban areas.

Each program has its own eligibility requirements, benefits, and limitations. The key advantage of government-backed mortgages is flexibility. They often allow lower down payments and more lenient credit requirements.

Key Differences You Should Consider

When deciding between conventional and government-backed home loans, focus on the factors that directly impact your finances.

Credit Score Requirements

If you have a strong credit score, usually 680 or higher, a conventional loan might offer better terms. Higher credit often translates to lower interest rates and reduced private mortgage insurance costs.

On the other hand, if your credit score is lower or you have limited credit history, an FHA loan can be more forgiving. Government-backed loans are designed to expand access to homeownership, especially for first-time buyers.

Down Payment Expectations

Conventional loans often require a higher down payment if you want the best rates. While some programs allow as little as 3% down, putting down 20% helps you avoid private mortgage insurance.

FHA loans typically require a smaller down payment, sometimes as low as 3.5%. VA loans may even allow zero down for qualified borrowers. USDA loans can also offer zero down options in eligible areas.

If saving for a large down payment feels overwhelming, a government-backed loan could make homeownership possible sooner.

Mortgage Insurance Costs

Mortgage insurance is another major factor when comparing home loan options.

With conventional loans, you may need private mortgage insurance if your down payment is less than 20%. The good news is that this insurance can usually be removed once you reach enough equity in your home.

FHA loans require mortgage insurance premiums, and in many cases, those premiums last for the life of the loan unless you refinance. This can increase your long-term costs.

VA loans do not require monthly mortgage insurance, but they do include a funding fee. USDA loans also include guarantee fees.

Over time, these differences can significantly affect how much you pay overall.

Loan Limits and Property Requirements

Conventional loans generally have higher loan limits compared to FHA loans in many areas. If you’re purchasing a more expensive property, this may matter.

Government-backed loans can have stricter property requirements. FHA loans, for example, require the home to meet certain safety and livability standards. USDA loans restrict properties to designated rural or suburban areas.

If you’re buying a unique property or a higher-priced home, a conventional mortgage might provide more flexibility.

When a Conventional Loan Makes Sense

A conventional mortgage can be a smart choice if you have strong financial credentials. Borrowers with stable income, low debt, and good credit often benefit from competitive interest rates and fewer long-term fees.

It also makes sense if you can afford a larger down payment. Avoiding private mortgage insurance can save you thousands over the life of the loan.

Additionally, if you plan to stay in your home long term and want to minimize total borrowing costs, conventional financing can offer more control and flexibility.

When a Government-Backed Loan Is the Better Option

Government-backed home loans are ideal for borrowers who need more flexibility.

If you’re a first-time homebuyer with limited savings, an FHA loan can lower the barrier to entry. If you’re eligible for a VA loan, the benefits can be substantial, especially with no down payment and no monthly mortgage insurance.

USDA loans are attractive for buyers in rural areas who meet income limits and want to purchase with little to no down payment.

These programs are designed to make homeownership accessible. For many families, they are the stepping stone that turns renting into owning.

How to Make the Final Decision

Choosing between conventional and government-backed home loans ultimately comes down to your financial profile and future goals.

Start by reviewing your credit score and calculating your debt-to-income ratio. Estimate how much you can comfortably afford for a down payment. Consider how long you plan to stay in the home.

It’s also wise to compare loan estimates from multiple lenders. Interest rates, fees, and qualification standards can vary. Even within the same loan type, offers may differ.

Take your time. Ask questions. Understand the total cost over the life of the loan, not just the monthly payment.

Final Thoughts

There is no one-size-fits-all answer when it comes to choosing between conventional and government-backed home loans. Both options have advantages and trade-offs.

Conventional mortgages often reward strong credit and financial stability with competitive terms. Government-backed loans provide flexibility and accessibility, especially for first-time buyers, veterans, and rural homeowners.

The key is aligning the loan type with your personal financial situation. When you understand the differences in credit requirements, down payments, mortgage insurance, and eligibility rules, you can move forward with confidence.

Buying a home is a major milestone. With the right mortgage strategy, it can also be a smart financial move that supports your long-term goals.